The Congressional Budget Office has put out a report on "Trends in the Distribution of Household Income Between 1979 and 2007." It's a treasure trove of useful figures and explanations. I can't resist offering a bunch of highlights, which I will divide into three posts--with this as the first one.

The gains to the top 1% of the income distribution.

An explanation of the Lorenz curve and the Gini coefficient, for those who would like to understand some terminology that is often used when discussing inequality.

The basic concept of the top 1% ranked by annual income is often muffed in the media. For example, a Washington Post headline about this report read: "Nation’s wealthiest 1 percent triple their incomes, according to CBO report." This is incorrect in two ways. First, wealth is what you have accumulated over time, so it is is not the same as income, which is what is received in a given year. The CBO report says nothing about the "wealthiest" 1 percent. Second, referring to the top 1% as a fixed group is incorrect. who is in the top 1 percent will change over time, especially over the period of nearly three decades from 1979-2007. Some people make the top 1% when they get a big annual bonus, but not other years. For example, think about those in the top 1% who were in the 45-50 age bracket in 2007. Back in 1979, they would have been 28 years younger, in the 17-22 age bracket, and very few of them would have been in the top 1% of income at that time. Conversely, those who were in the top 1% and the 45-50 age bracket in 1979 would be 28 years older by 2007, and many of those in the 73-78 age bracket would have retired.

While it is certainly true that the top 1% is a group that evolves over time, this point shouldn't be pushed too hard. Inequality as measured by annual income is rising; however, I don't know of any evidence that mobility between broad income groups has been rising. Greater inequality isn't being offset by greater mobility.

Here's a graph showing the cumulative percentage growth in after-tax, after-transfer income for various income groups, measured on an annual basis. Income growth is slowest for t hose in the lowest quintile (or fifth) of the income distribution, and then faster in ascending order for those in the 21st to 80th percentiles, the 81st to 99th percentiles, and the top 1%. The percentage gains for the top 1% are remarkably higher than for the other groups.

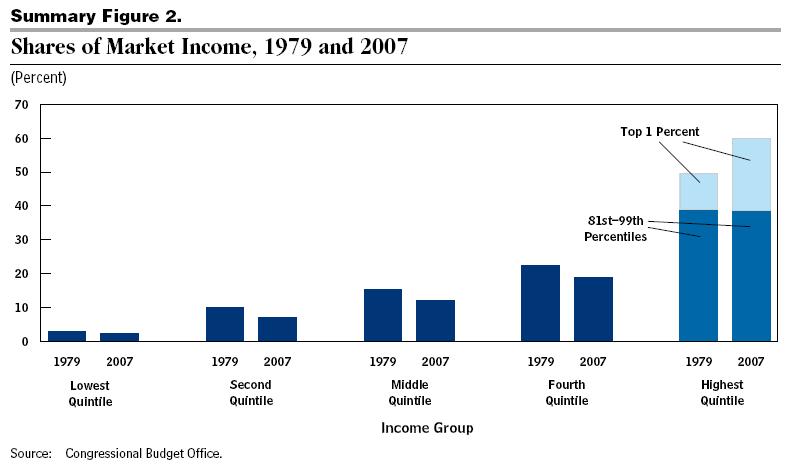

One can look at this underlying data in a different way: What share of total market income did these groups receive in 1979, compared to 2007? And what share of after-tax, after-transfer income did these groups receive in 1979, compared to 2007? The timeframe is a useful one, because it runs from one business cycle peak just before a deep recession in 1979 to another year that is a business cycle peak just before a deep recession. Thus, patterns over this time can't be attributed to comparing a recession year to a nonrecession year. The overall pattern is fairly clear. Whether looking at market income or at after-tax, after-transfer income, the 80th-99th percentile received about the same share of income in 2007 as in 1979. The top 1% got a notably larger share. Each of the lower four-fifths of the income distribution got a lower share.

There is a modest rise in inequality of annual incomes even leaving out the top 1%, but most of the increase in annual income inequality is being driven by rising incomes of the top 1%. It's perhaps useful to add that pointing out the fact of rising inequality doesn't say anything about underlying causes or possible policies.

For a July 18 post on causes of inequality, see "Causes of Inequality: Supply and Demand for Skilled Workers." For an overview of philosophical and economic arguments about inequality, see the September 30 post, "A Critique of the Arguments for Inequality."

In a hedged and roundabout way, the Vatican has endorsed a financial transactions tax. The announcement came in a Note on financial reform from the Pontifical Council for Justice and Peace , which is one branch within the official governing structure of the Catholic Church. The Note advocates a "world Authority" and "global monetary management," but also admits: "However, a long road still needs to be travelled before arriving at the creation of a public Authority with universal jurisdiction." When the note gets down to more immediate suggestions, it offers three:

"On the basis of this sort of ethical approach, it seems advisable to reflect, for example, on: a) taxation measures on financial transactions through fair but modulated rates with charges proportionate to the complexity of the operations, especially those made on the “secondary” market. Such taxation would be very useful in promoting global development and sustainability according to the principles of social justice and solidarity. It could also contribute to the creation of a world reserve fund to support the economies of the countries hit by crisis as well as the recovery of their monetary and financial system; b) forms of recapitalization of banks with public funds making the support conditional on “virtuous” behaviours aimed at developing the “real economy”; c) the definition of the domains of ordinary credit and of Investment Banking. This distinction would allow a more effective management of the “shadow markets” which have no controls and limits."

I will sidestep here the second and third points, on what it means to have "virtuous" bankers who develop the "real economy" and what kind of financial regulation is appropriate for all the institutions in a modern economy. But on the issue of a financial transactions tax, Thornton Matheson of the IMF offers a nice review of the economics of "Taxing Financial Transactions: Issues and Evidence" in Working Paper WP/11/54 released last March. Here are a few highlights (footnotes and citations omitted):

Financial transactions have increased substantially

"Transaction costs have indeed fallen dramatically across financial markets over the past 35 years due to advances in information technology, deregulation, and product innovation. In the U.S. equity market, commission deregulation (1975) and decimalization (2000) both substantially lowered transactions costs. Bid/ask spreads on the NYSE now average about 0.1 percent, vs. 1.3 percent in the mid-1980s. In the foreign exchange market, bid-ask spreads for major currencies are currently as little as 1–4 basis points, half the level of a decade ago. Spreads in interest rate futures and swaps are also on the order of a few basis points. Development of the interest rate and credit default swap markets has enabled investors to tailor their fixed-income exposure more cheaply than by trading the underlying bonds."

"As economic theory would predict, this steep decline in financial transaction costs has produced an increase in financial transactions relative to real activity. The value of world financial transactions, which was 25 times world GDP in 1995, rose to70 times that value by 2007. The growth of transactions has been concentrated in derivatives markets, which often have much lower transaction costs relative to notional values than spot markets. Growth in interest rate and equity derivatives transactions has far outstripped growth in business investment in North America and Europe, while the ratio of spot transactions to investment has remained fairly steady. As theory would also predict, lower transactions costs have particularly spurred short-term trading. The past decade has witnessed explosive growth in algorithm or computer-driven trading that relies on high-speed transactions. In 2009, algorithm trading accounted for at least 60 percent of U.S. equity trading volume (up from about 30 percent in 2006), and 30–40 percent of European and Japanese equity trading. Algorithm trading also accounts for 10–20 percent of foreign exchange trading volume, 20 percent of U.S. options volume, and 40 percent of U.S. futures volume."

Many countries already have some version of a financial transactions tax at a low level

In the United States, for example: " The United States’ Securities and Exchange Commission (SEC), its equity market regulator, imposes a 0.17 basis point chargeon stock market transactions to fund its regulatory operations. ... New York State levies a tax of up to five cents per share on within-state stock trades with a cap of $350 per trade ..." However, the trend in recent decades is that the level of such taxes has been dropping around the world.

The case for a financial transactions tax is weak

"The potentially large base of an STT [security transactions tax] promises an opportunity to raise substantial revenue with a low-rate tax. Current estimates of the revenue potential of a low-rate (0.5–1 basis point) multilateral CTT [currency transactions tax] on the four major trading currencies suggest that it could raise about $20–40 billion annually, or roughly 0.05 percent of world GDP. A one basis point STT on global stocks, bonds and derivatives is estimated to raise approximately 0.4 percent of world GDP.

"However, financial transactions taxes create many distortions that militate against using an STT to raise revenue. STTs reduce security values and raise the cost of capital for issuers, particularly issuers of frequently traded securities. STTs also reduce trading volume: studies of existing STTs and other transaction costs suggest that the elasticity of trading volume with respect to transactions costs ranges broadly between -0.4 and -2.6, depending on the market studied. Markets with products for which there are more untaxed substitutes, such as derivatives or foreign listings, have higher elasticities. Lower trading volume in turn reduces liquidity and slows price discovery.

"An STT is also an inefficient instrument for regulating financial markets and preventing bubbles. There is no convincing evidence that STTs lower short-term price volatility, and high transaction costs are likely to increase it. Current economic thought attributes asset bubbles to excessive leverage, not excessive transactions per se. ...

"The short-run incidence of an STT would likely be quite progressive, as securities values fell in response to the tax. Financial activity, particularly short-term trading, would contract, lowering financial sector profits. Financial firms would likely pass the cost of an STT on surviving activity on to clients, which include not only wealthy individuals and corporations but also charities and pension and mutual funds. In the medium term, release of resources from the financial sector could lower the equilibrium return to highly skilled labor. In the long run, the burden of an STT depends on the elasticity of the capital supply: Like the corporate income tax, the higher financing costs imposed by an STT will fall more heavily on labor than on capital owners as the elasticity of the supply of capital increases."

This last argument points out that in the long run, if a financial transactions tax makes it more costly to raise capital, then it will lead to a capital stock that is lower than it would otherwise be. As a result, workers in that country who have less capital with which to work will end up bearing the burden of the tax.

If the goal is to discouraging asset bubbles, tax changes to discourage leverage are more appropriate

"To discourage leverage at the institutional level, a tax on balance sheet debt (net of insured deposits and equity), such as the financial sector contribution (FSC), could be used. The FSC could be tailored to tax systemically important institutions more heavily, since their risks pose a greater danger to the broad economy. Another means of combating leverage at the firm level is reform of the corporate income tax (CIT), which

encourages debt over equity finance due to its disparate treatment of interest and earnings. To discourage debt finance while raising revenue, interest deductibility could be reduced or even eliminated, as in a comprehensive business income tax ..."

If the goal is to raise tax revenue from the financial sector, think VAT or FAT

"To tax the financial sector, the base of an existing VAT [value-added tax] could be broadened to include fee-based financial services, or an FAT could be introduced." A FAT is a “financial activities tax,” which would be levied on the sum of financial institutions profits and wages.

Jeffrey Frankel has a readable overview of the arguments over "The Curse: Why Natural Resources are Not Always a Good Thing," in the Fourth Quarter 2011 issue of the Milken Institute Review, available (with free registration) here. Frankel writes:

"It is striking how often countries that are rich with oil, minerals or fertile land have failed to grow more rapidly than those without. Angola, Nigeria and Sudan are all awash in petroleum, yet most of their citizens are

bitterly poor. Meanwhile, East Asian economies, including Japan, Korea, Taiwan, Singapore and Hong Kong, have achieved Western-level standards of living despite being rocky islands (or peninsulas) with virtually no exportable natural resources. This is the phenomenon known to economists as the “natural resources curse.” The evidence for its existence is more than anecdotal. The curse shows up in econometric tests of the determinants of economic performance across a comprehensive sample of countries.

Consider the figure on page 31, which plots the relationship between nonagricultural resource exports as a portion of total goods exports and average economic growth rates over the past four decades. The usual

suspects – China, Korea, Thailand – are conspicuously high in growth and low in natural resources. Likewise, resource-rich Liberia, Venezuela and Zambia have little to show for their wealth in terms of economic development. The negative correlation is not very strong because some countries – think Chile and Saudi Arabia – have managed to have it both ways. But the data certainly suggest no positive correlation between natural resource wealth and economic growth."

Frankel offers a wide array of examples and evidence on the natural resources curse. Along the way, he reviews the possible reasons why natural resources might hinder economic growth: 1) Commodity prices fluctuate a lot, so an economy that depends on commodity exports will be hit by a series of shocks; 2) An economy focused on natural resources diverts land, labor, and capital from other sectors of the economy, like manufacturing; 3) Natural resource endowments can foster corruption and weak institutions, as different groups jostle for control of the income from the resources; 4) High exports of natural resources can lead to currency appreciation which then disadvantages all other exports; and 5) Natural resources can be depleted.

He also discusses policies that countries can use to reduce the risk of these pitfalls.

• Hedge export proceeds on derivatives markets (in particular, options markets), as Mexico has done with oil. That way, exporting countries can plan government budgets around firm expectations of revenues and, as important, dampen shocks caused by unanticipated changes in price.

• Denominate debt in terms of the world price of the export commodity. Exporting countries can (and, in some cases, should) borrow abroad, for example, to develop infrastructure. By writing debt contracts in which the principal is indexed to the price of their export commodity, borrowing countries can share the risk of commodity price volatility with lenders. ...

• Adopt Chilean-style fiscal rules, which prescribe a structural budget surplus and use independent panels of experts to determine what future price of the export commodity – in Chile’s case, copper – should be assumed in forecasting the structural budget. Thus, when the independent experts determine that copper prices have fallen below long-term expectations, the government is authorized to offset the impact with temporary fiscal stimulus. But when copper prices are above the long term trend, and the bonanza is determined to be entirely temporary, the government must save the proceeds.

• Intervene in foreign exchange markets to dampen upward pressure on an exporter’s currency in the early stages of commodity booms, while seeking to prevent the money supply from swelling. Subsequently, allow gradual appreciation when the commodity boom has proved to be long-lived or when domestic inflation is no longer contained.

• Establish transparent sovereign wealth funds with the proceeds of commodity exports in order to assure that future generations share the bounty. Botswana’s Pula Fund, built on earnings from the sale of diamonds, is a good model. The fund, invested entirely in securities denominated in other currencies, serves both as a sinking fund to offset the depletion of diamonds and as a buffer to smooth economic fluctuations.

• Make lump-sum per capita distributions of revenues from mineral exports in order to make sure the money doesn’t end up in the bank accounts of corrupt officials.

Every introductory course in economics points out that rational actors should ignore sunk costs: look forward at costs and benefits, not backward at things that can't be changed. But in the November 2011 issue of the American Economic Journal: Microeconomics, Sandeep Baliga and Jeffrey C. Ely offer an argument as to why rational actors should pay attention to sunk costs in "Mnemonomics: The Sunk Cost Fallacy as a Memory Kludge." Those who want the mathematical model and details on the follow-up laboratory experiment need to go through a library to get the article. But in the opening pages, the authors do a nice job of providing the basic intuition.

They start with a reminder of some of the classic evidence on people paying attention to sunk cost: theater tickets and production of the Concorde supersonic jet. They write: "In a classic experiment, Hal R. Arkes and Catherine Blumer (1985) sold theater season tickets at three randomly selected prices. Those who purchased at the two discounted prices attended fewer events than those who paid the full price. Hal Arkes and Peter Ayton (1999) suggest those who had “sunk” the most money into the season tickets were most motivated to use them. R. Dawkins and T. R. Carlisle (1976) call this behavior the Concorde effect. France and Britain continued to invest in the Concorde supersonic jet after it was known it was going to be unprofitable. This so-called “escalation of commitment” results in an over-investment in an activity

or project."

Here is their argument for why paying attention to sunk costs can make sense: "We provide a theory of sunk cost bias as a substitute for limited memory. We consider a model in which a project requires two stages of investment to complete. As new information arrives, a decision-maker or investor may not remember his

initial forecast of the project’s value. The sunk cost of past actions conveys information about the investor’s initial valuation of the project and is therefore an additional source information when direct memory is imperfect. This means that a rational investor with imperfect memory should incorporate sunk costs into future decisions. ... If the investor has imperfect memory of his profit forecast, a high sunk cost signals that the forecast was optimistic enough to justify incurring the high cost. For example, the willingness to incur a high sunk cost digging dry wells may signal that the oil exploration project is worth continuing. If this is the main issue the investor faces, it generates the Concorde effect as he is more likely to continue a project which was initiated at a high cost."

They point out various ways in the real world that this dynamic--that is, imperfect information about why a decision was made in the past--can cause current actors to treat sunk costs as useful information. "There are a few different ways these effects can manifest themselves in practice. Most directly, the decision maker may be an individual responsible for making the initiation and continuation decision and he may simply forget the information. An organization may also forget information or knowledge. Managerial turnover can generate organizational forgetting. In this case, we can think of the investor in the model as representing a long-lived organization headed by a sequence of short-term executives. An executive who inherits an ongoing project will not have access to all of the information available at the time of planning. Existing strategies and plans will then encode missing information and a new executive may continue to implement the plans of the old executive. In our model, data about sunk costs partially substitutes for missing information and a rational executive takes this into account."

Finally, and intriguingly, they suggest that paying attention to sunk costs may be hard-wired into people's brains as an adaptive mechanism. "Finally, we can think of sunk-cost bias as a kludge: an adaptive heuristic wherein metaphorical Nature is balancing a design tradeoff. ... In our model, the sunk cost bias is an optimal heuristic that compensates for the constraints of limited memory. This can explain the prevalence and persistence of sunk-cost bias despite its appearance, superficially, as a fallacy. To the extent that heuristics are hard-wired or built into preferences, the sunk-cost bias in observed behavior would be adapted to the “average” environment but not always a good fit in specific situations. For example, we would expect that decision-makers display a sunk-cost bias even when full memory is available, and that sometimes the bias goes in the wrong direction for the specific problem at hand."

On this final point, I'm not yet persuaded. But many economic decisions do unfold over time, and many of them may have a period of disutility or losses early in the process, later followed by compensating utility or gains. It would clearly be misguided to make a choice to pursue a path over time, then when partway into the process to forget about or undervalue the gains to come.

Jeremy Gerst and Daniel J. Wilson of the Federal Reserve Bank of San Francisco have a short essay:

"What's in Your Wallet? The Future of Cash." They offer evidence for the intriguing fact that in an economy with increasing use of credit cards, debit card and electronic transfers, the amount of cash outstanding has kept growing. But they don't tackle what to me is the most intriguing question in this area: Who is holding all this currency?

Facts first. As Gerst and Wilson write: "Over the past few decades, the dominant position of cash as a store of value and a means of payment has increasingly been challenged. The growth of electronic payments, especially credit cards and, more recently, debit cards, has radically changed the role of cash in the global economy. Yet, the circulation of the U.S. dollar, the world’s most widely used currency, has continued to grow without interruption. Last year, the value of U.S. currency in circulation reached nearly $1 trillion dollars."

Gerst and Wilson offer a figure to describe the rise in currency in circulation, and describe it this way: "First,

currency in circulation has grown around a steady trend with minimal fluctuations throughout this period.

Despite dramatic changes in the payment landscape over the past 30 years and the recent financial crisis and

recession, cash holdings among households, businesses, and banks have continued to grow at a steady pace.

Second, around 2005 and 2006, the Fed’s gross shipments of cash began to diverge sharply from currency in circulation. Cash shipments fell steeply, while currency in circulation continued to grow. In other words, banks sharply reduced the value of cash they sent to the Fed for processing, but continued to order more new cash than they returned, so that currency in circulation grew. The divergence between Fed cash shipments and currency in circulation was probably due to a recirculation policy that the Fed instituted in 2006 to discourage banks from overusing the Fed’s free cash-processing service. The policy applied specifically to $10 and $20 notes. Indeed, the steep drop in cash volumes was unique to those two denominations ..."

Gerst and Wilson offer some estimates and simulations about trends in cash payments and demand for cash in the future. But to me, the more interesting question is who is holding all that cash. In my Principles of Economics textbook, available from Textbook Media (and of course I encourage all those teaching an introductory economics course to check it out), I included a discussion box on this question in Chapter 29 on "Money and Banking." The cash total cited here is from a few years ago, but the basic message remains. I'll quote from the textbook here:

The Case of the Missing Currency

Here is a puzzle. The Federal Reserve reported that about $800 billion in currency—that is, paper money and coins—was in circulation in 2006. Dividing the total currency by roughly 210 million U.S. adults over the age of 18 works out to an average of approximately $3,800 in currency for every man and woman.

This average seems ridiculously high. Survey results suggest that the average holdings of currency for each adult are more like $350—and that number takes into account well-off people who hold large amounts of cash in safes and safety deposit boxes. If 210 million adults are each holding $350, then total holdings of U.S. currency by individuals is about $73 billion. Businesses traditionally hold about 3% of all currency, or about $24 billion. After all, most businesses try not to hold currency, but instead quickly get money to the bank where it can earn some interest.

So if households and firms together hold about $97 billion in currency, where is the other $703 billion? No one is quite sure. There are three possible answers: it may be held by children; as part of the unmeasured “underground” economy; or by foreigners. Even if one believes that teenage buying power is important to certain sectors of the economy, and that underground, unreported businesses are everywhere, it is very hard to believe that these two components are larger than the uses of money by adults and legal businesses. As a result, it seems likely that hundreds of billions of dollars of U.S. currency is circulating in the hands

of foreigners. When a country’s own currency is plagued with uncertainty, perhaps because of a high inflation rate, people in that country may start carrying out transactions and saving money by using U.S. dollars.

But this explanation is not completely satisfactory either. In high-income economies like those of the European nations, Japan, and Canada, people have relatively little need to use U.S. currency for transactions or saving. People may invest in the United States, but they can do so with electronic money; they don’t need actual currency in the form of paper and coins. In the middle and low-income countries of the world, the average

families are too poor to account for hundreds of billions of dollars of U.S. currency.

The case of the missing currency remains unsolved.

I would be remiss if I didn't add that I first learned about "The Case of the Missing Currency" from an article by Case Sprenkle in the Fall 1993 issue of my own Journal of Economic Perspectives. The journal is freely available from the most recent issue back to around 1998, but this is a little too far back to be freely available online. However, it's readily available if you search the web, as well as on JSTOR.

The Drill-Baby Carbon Tax is my proposed grand compromise for energy policy in the United States. As the name suggests, it has two parts. On one side, there would be a national commitment to move ahead with all deliberate speed in developing the vast U.S. fossil fuel energy resources that are now technologically available. On the other side, the United States would enact a appropriate carbon tax to offset concerns over the risks of climate change. The Drill Baby Carbon Tax basically takes the view that while the United States is working on phasing down fossil fuels and moving to alternative energy resource, let's produce a greater share of the fossil fuels that we consume here at home.

Personally, I like both sides of the Drill Baby Carbon Tax. But for many, it's a proposal with something to like and something to loathe. Is there any chance for at least some environmentalists and some of those who favor aggressively developing our domestic energy resources to support such a compromise?

A number of environmentalists have been warning about the dangers of climate change in near-apocalyptic terms. If it is, as often claimed, the preeminent environmental issue our time with a risk of extraordinarily large and even catastrophic costs, then surely a carbon tax should be worth accepting some other tradeoffs.

At a more subtle level of argument, many environmentalists would be horrified by a proposal that would involve taking pollution from U.S. and dumping it elsewhere; but after all, a policy in which the U.S. burns imported fossil fuel is only saving environmental costs in the U.S. while imposing them elsewhere. From a global environmental perspective, if fossil fuel resources are to be developed, better that it happen here under the eye of U.S. regulatory agencies and courts and everyday U.S. citizens, rather than in Nigeria or Russia. Moreover, if energy development was happening in America, U.S. citizens would need to face the reality of what they are using.

By trying to block, for example, a pipeline from Canada that would bring oil from the "tar sands" to the U.S., environmentalists are missing the fact that these resources are going to be developed somewhere in the world--and carbon emissions are the bigger issue. For example, Nature magazine editorialized in its September 15 issue: "In fact, the pipeline protests say more about the sorry state of the environmental agenda than anything else. It is true that greenhouse-gas emissions from oil extracted from the sands are 15–20% higher than those from average crude oil if assessed on a life-cycle basis, but industry officials are correct in pointing out that this is on a par with other dirty oils produced in the United States and elsewhere using steam injection. And halting this pipeline is unlikely to halt development of the tar sands or other dirty sources of energy. What is missing, now as ever, is a policy to address the larger climate threat."

For those in favor of developing U.S. domestic energy resources, it's important to be clear such a policy isn't going to have much affect on the average price over time, which is set in a global market of supply and demand. However, oil produced in North America is less susceptible to disruptions and cutoffs that can cause sharp fluctuations in world prices and stagger economies. If more oil was produced here, there would be less reason for a U.S. military presence in the Middle East, and fewer trigger points for conflict over oil around the world. Perhaps most important, if oil is going to be produced somewhere, having it produced and refined by U.S. workers creates jobs here, rather than having the U.S. run a large trade deficit in part because of importing oil produced somewhere else.

Of course, many of those who favor expanding domestic oil drilling don't think the evidence for climate change is very strong, and don't think a carbon tax is justified. But essentially everyone acknowledges that burning fossil fuels creates standard pollutants: sulfur oxides, nitrogen oxides, particulate matter, and the like. Even if reducing carbon emissions is unimportant, reducing these other pollutants has some gains. The distaste for a carbon tax would also have to be weighed against the gains from additional U.S. jobs, a less volatile world energy supply, less pressure to seek political stability in the Middle East, and a lower U.S. trade deficit. And for advocates of developing domestic energy resources, imagine the political power of generously offering a grand compromise that might co-opt and defang the climate change issue!

What might the specific dimensions of the Drill Baby Carbon Tax look like? On the production side, the concrete and goal would be how much the U.S. ramped up its domestic fossil fuel production. Earlier this month, I blogged on "America as a Conventional Energy Powerhouse?", where an energy expert predicts that thanks to horizontal drilling and other technological developments, "[b]y the 2020s, the capital of energy will likely have shifted back to the Western Hemisphere ..." The process here would be make sure that environmental regulations are met, but not to let those regulations be used to shut off developing these fossil fuel resources.

On the carbon tax side, the question is how large a tax is justified by the existing scientific evidence. A useful starting point here is a paper by three economists: Michael Greenstone of MIT and Elizabeth Kopits and Ann Wolverton of the EPA. All three of them participated in a group that tried to calculate a social cost of carbon for the federal government. (Greenstone was Chief Economist on the staff of Obama's Council of Economic Advisers in 2009 and part of 2010.) In March 2011, they published a working paper on "Estimating the Social Cost of Carbon for Use in U.S. Federal Rulemakings: A Summary and Interpretation."

The social cost of carbon (SCC) depends to some extent on what discount rate one uses. A higher discount rate makes future costs less salient in the present, and vice versa. They write (footnotes omitted): "For 2010, the central value is $21 per ton of CO2 emissions and sensitivity analysis is to be conducted at $5, $35, and $65. The $21, $5, and $35 values are based on the average SCC across the models and scenarios examined for the 5, 3, and 2.5 percent discount rates, respectively. The $65 value—the 95th percentile of the SCC distribution at a 3 percent discount rate—was chosen to represent potential higher-than-expected impacts from temperature change.These SCC estimates also grow over time based on rates endogenously determined within each model. For instance, the central value increases to $24 per ton of CO2 in 2015 and $26 per ton of CO2 in 2020."

For economists, of course, a natural approach is to phase in a carbon tax at the level that matches the social cost of carbon, so that users of fossil fuels need to pay the social costs that they are imposing, and will have an incentive to adjust their behavior accordingly. How much of a boost would a carbon tax at these levels cause to, say, gasoline prices? A Congressional Budget Office Report from October 2008 looked at "Climate-Change Policy and CO2 Emissions from Passenger Vehicles." The CBO estimate is that a carbon tax at $28/ton of carbon would add about 25 cents/gallon to the price of gasoline--if gas is $4/gallon, this would be a price increase of about 6%. A carbon tax would also affect coal and natural gas, so those prices would rise as well. This price increase is certainly noticeable; after all, part of the point is to provide incentives to developing non-carbon sources of energy. But on the other side, after the gas and energy price fluctuations of the last few years, it is hardly an unprecedented change for Americans to handle. U.S. gasoline prices, for example, would still be far below the levels common in Europe. In early October, the U.S. Energy Information Administration reported that the average U.S. price for a gallon of regular gas was $3.70, compared with almost $8/gallon in Germany, France, Italy, and the United Kingdom.

Of course, I'm well aware that the Drill Baby Carbon Tax would be hard to legislate. At least some of the same environmentalists who complain that people are highly reluctant to believe the science of climate change will be themselves highly reluctant to accept the evidence that a realistic carbon tax should be set at this level--and instead will want something truly punitive. At least some of the those who favor additional development of U.S. fossil fuel resources will be dead set against a tax that would raise the price of this energy. There would be dispute over how to use the $100 billion or more in likely revenues from a carbon tax of $20-25 per ton of carbon: for example, these revenues could be used as part of a package for long-run reduction of budget deficits, or could finance cuts in other taxes. It would probably be necessary to yoke the rising domestic fossil fuel production and the rising carbon tax together, so neither one could increase without the other increasing as well.

But while the practical details are daunting, perhaps this is one of the rare cases where for both extremes, the prize is worth the compromise. And I suspect that plenty of folks in the middle might buy into the grand compromise of the Drill Baby Carbon Tax.

Traditionally, households were billed for electricity at a flat rate. You could make investments in energy conservation, and the savings would be the quantity of electricity saved multiplied by that flat rate. But in the wholesale market, electricity rates fluctuate a great deal. When demand is highest, the system operators need to bring expensive "peaking" power plants on-line, and prices jump. With new "smart meter" technology, it is becoming possible for consumers to react to these fluctuations in electricity prices. In "Dynamic Pricing and Its Discontents" in the Fall 2011 issue of Regulation magazine, Ahmad Faruqui and Jennifer Palmer offer a nice readable overview of the possibilities. If you're teaching a basic economics class and looking for a nice vivid modern real-word example of consumers adjusting to price changes that doesn't involve hypothetical pizzas and haircuts, electricity pricing might be a good choice.

Here's the underlying issue that causes wholesale electricity prices to fluctuate: "Since electricity cannot be stored and has to be consumed instantly on demand, and since demand fluctuates based on lifestyle and weather conditions, the electric system typically has to keep spare “peaking” generation capacity online for

times when demand may surge on short notice. Often, these “peaking” power plants are only run for 100–200 hours a year, adding to the average cost of providing electricity. Dynamic pricing incentivizes electricity consumers to lower their usage during peak times, especially during the top 100 “critical” hours of the year, which can account for anywhere from 8 to 18 percent of annual peak demand."

Smart meters are coming: "By 2015, according to the Institute of Electric Efficiency, about half of the nation’s 125 million residential customers will have smart meters. The institute anticipates that by 2020, nearly all customers will be on smart meters. Thus, a major technical barrier to dynamic pricing should be lifted in the next five to 10 years."

Consumers respond when faced with variable prices: "However, almost all analyses of pilot results show that customers do respond to dynamic pricing rates by lowering peak usage. Indeed, in 24 different pilots involving a total of 109 different tests of time-varying rates — covering many different locations, time periods, and rate designs — customers have reduced peak load on dynamic rates relative to flat rates, with a median peak reduction (or demand response) of 12 percent.... In other words, the demand for electricity does respond to price, just like the demand for other products and services that consumers buy."

Consumers who have better technology to adjust their electricity use react more strongly: "During the past few years, a variety of new technologies have been introduced to help customers understand their usage patterns (through web portals and in-home displays, for example), to automatically control the function of their major end-uses such as central air conditioning and space heating equipment (smart thermostats), and to manage all their other appliances and plug-loads (home energy management systems). ... Looking across all 39 pilot results with enabling technologies, the median peak reduction is 23 percent, 9 percentage points

higher than the median across all 109 results."

Many low-income customers would benefit from dynamic pricing: "Some people speculate that because low-income customers typically use less power, they have little discretion in their power usage and are thus unable to shift load depending on price. As a result, low income customers would be hurt by dynamic pricing.

However, empirical evaluation of this speculation has indicated that most low-income customers would immediately save money on their electricity bills from dynamic pricing. In general, when customers are placed on a revenue-neutral dynamic rate, we expect roughly half of the customers to immediately see bill increases and half to see bill decreases. Customers who use more load in the peak hours than the average customer would see higher bills, while customers who use less load in the peak hours than the average customer would see lower bills. ... Because the low-income customers tend to have flatter load shapes, roughly 65 percent of the low-income customers were immediately better off on the CPP [critical peak pricing] rate than on the flat rate. In other words, even without any change in electricity usage, more than half of low-income customers are better off on a dynamic rate."

Total savings? "At the national level, an assessment carried out for FERC twoyears ago showed that the universal application of dynamicpricing in the United States had the potential for quintupling the share of U.S. peak demand that could be lowered through demand response, from 4 percent to 20 percent. Another assessment quantified the value of demand response and showed that even a 5 percent reduction in U.S. peak demand could lower energy costs $3 billion a year."

By the middle of 21st century, world population is likely to reach about 9 billion. Set aside for a moment all the other issues involved with this rise in population, and focus on this one: How will the world economy feed them all? A parade of authors led by Jonathan A. Foley offer "Solutions for a cultivated planet" in a paper published on-line in Nature on October 12, 2011 (subscription required). Here are some highlights (footnotes and references to figures omitted):

The authors lay out the challenge: "Recent studies suggest that production would need to roughly double to keep pace with projected demands from population growth, dietary changes (especially meat consumption), and increasing bioenergy use, unless there are dramatic changes in agricultural consumption patterns. Compounding this challenge, agriculture must also address tremendous environmental concerns. Agriculture is now a dominant force behind many environmental threats, including climate change, biodiversity loss and degradation of land and freshwater. ... Looking forward, we face one of the greatest challenges of the twenty-first century: meeting society’s growing food needs while simultaneously reducing agriculture’s environmental harm."

After offering a detailed and thoughtful analysis of the problem, they make four recommendations:

1) Stop expanding agriculture. They argue that the environmental destruction done by expanding agricultural land in a significant way, especially into tropical forests, is just too great to justify the increases in output that could result.

2) Close yield gaps. "Here we define a yield gap as the difference between crop yields observed at any given location and the crop’s potential yield at the same location given current agricultural practices and technologies. ... Closing yield gaps could substantially increase global food supplies. Our analysis shows that bringing yields to within 95% of their potential for 16 important food and feed crops could add 2.3 billion tonnes (5×1015kilocalories) of new production, a 58% increase. Even if yields for these 16 crops were brought up to only 75% of their potential, global production would increase by 1.1 billion tonnes (2.8×1015kilocalories), a 28% increase. Additional gains in productivity, focused on increasing the maximum yield of key crops, are likely to be driven by genetic improvements. Significant opportunities may also exist to improve yield and the resilience of cropping systems by improving ‘orphan crops’ (such crops have not been genetically improved or had much investment) and preserving crop diversity, which have received relatively little investment to date."

3) Increase agricultural resource efficiency. "Even though excess nutrients cause environmental problems in some parts of the world, insufficient nutrients are a major agronomic problem in others. Many yield gaps are mainly due to insufficient nutrient availability. This ‘Goldilocks’ problem of nutrients (that is, there are many regions with too much or too little fertilizer but few that are ‘just right’) is one of the key issues facing agriculture today."

4) Increase food delivery by shifting diets and reducing waste. "Simply put, we can increase food availability (in terms of calories, protein and critical nutrients) by shifting crop production away from livestock feed, bioenergy crops and other non-food applications. ... [W]e estimate the potential to increase food supplies by closing the ‘diet gap’: shifting 16 major crops to 100% human food could add over a billion tonnes to global food production (a 28% increase), or the equivalent of 3×1015 food kilocalories (a 49% increase). ... A recent FAO study suggests that about one-third of food is never consumed; others have suggested that as much as half of all food grown is lost; and some perishable commodities have post-harvest losses of up to 100%. Developing countries lose more than 40% of food post-harvest or during processing because of storage and transport conditions. Industrialized countries have lower producer losses, but at the retail or consumer level more than 40% of food may be wasted."

Their bottom line: "Our analysis demonstrates that four core strategies can—in principle—meet future food production needs and environmental challenges if deployed simultaneously. Adding them together, they increase global food availability by 100–180%, meeting projected demands while lowering greenhouse gas emissions, biodiversity losses, water use and water pollution."

Here are two other places to turn for useful takes on this topic:

The Economist magazine did one of its consistently excellent "Special Reports" on the subject of "Feeding the World: The Nine Billion People Question" in the February 24, 2011 issue. The essay is written by John Parker. Here's a brief flavor of his argument:

"An era of cheap food has come to an end. A combination of factors—rising demand in India and China, a dietary shift away from cereals towards meat and vegetables, the increasing use of maize as a fuel, and developments outside agriculture, such as the fall in the dollar—have brought to a close a period starting in the early 1970s in which the real price of staple crops (rice, wheat and maize) fell year after year. This has come as a shock. ...

The end of the era of cheap food has coincided with growing concern about the prospects of feeding the world. Around the turn of 2011-12 the global population is forecast to rise to 7 billion, stirring Malthusian fears. The price rises have once again plunged into poverty millions of people who spend more than half their income on food. The numbers of those below the poverty level of $1.25 a day, which had been falling consistently in the 1990s, rose sharply in 2007-08. That seems to suggest that the world cannot even feed its current population, let alone the 9 billion expected by 2050. Adding further to the concerns is climate change, of which agriculture is both cause and victim. So how will the world cope in the next four decades?...

feeding the world in 2050 will be hard, and business as usual will not do it. The report looks at ways to boost yields of the main crops, considers the constraints of land and water and the use of fertiliser and pesticide, assesses biofuel policies, explains why technology matters so much and examines the impact of recent price rises. It points out that although the concerns of the critics of modern agriculture may be understandable, the reaction against intensive farming is a luxury of the rich. Traditional and organic farming could feed Europeans and Americans well. It cannot feed the world."

In my own Journal of Economic Perspectives, Vernon Ruttan published "Productivity Growth in World Agriculture: Sources and Constraints," in the Fall 2002 issue. Vern had some interesting personal history here. As he told me, one of his earliest papers back in the mid-1950s looked at Malthusian predictions for whether it would be possible to feed the world over the next half-century from that time. He argues persuasively--and as it turned out, correctly--that it would be straightforward to feed the world in the second half of the 20th century with a combination of expanding agricultural land, improved irrigation and fertilizer, and technological progress. However, when Vern sat down around the year 2000 to do the same exercise, he found that it was much harder to be optimistic about feeding the world over the NEXT 50 years. Here's how Vern concluded his essay (references omitted):

"While many of the constraints on agricultural productivity discussed in this paper [like soil, water, pest control and climate] are unlikely to represent a threat to global food security over the next half-century, they will, either individually or collectively, become a threat to growth of agricultural production at the regional and local level in a number of the world’s poorest countries. A primary defense against the uncertainty about resource and environmental constraints is agricultural research capacity. The erosion of capacity of the international research system will have to be reversed; capacity in the presently developed countries will have to be at least maintained; and capacity in the developing countries will have to be substantially strengthened. Smaller countries will need, at the very least, to strengthen their capacity to borrow, adapt and diffuse technology from countries in comparable agroclimatic regions. It also means that more secure bridges must be built between the research systems of what have been termed the “island empires” of the agricultural, environmental and health sciences.

If the world fails to meet its food demands in the next half-century, the failure will be at least as much in the area of institutional innovation as in the area of technical change. This conclusion is not an optimistic one. The design of institutions capable of achieving compatibility between individual, organizational and social objectives remains an art rather than a science. At our present stage of knowledge, institutional design is analogous to driving down a four-lane highway looking out the rear-view mirror. We are better at making course corrections when we start to run off the highway than at using foresight to navigate the transition to sustainable growth in agricultural output and productivity."

The TIGTA report sets the stage: "On March 23, 2010, the Patient Protection and Affordable Care Act (Affordable Care Act) was signed into law. Along with amendments in the Health Care and Education Reconciliation Act of 2010, which was signed on March 30, 2010, this legislation contains revenue provisions anticipated to generate $438 billion in the form of new taxes, fees, and penalties. One of these new taxes is an excise tax on indoor tanning services (referred to hereafter as the tanning tax)."

Apparently this was a 10% excise tax on tanning services, to be paid by the customer, collected by the business, and the forwarded along to the U.S. government quarterly. "According to IRS documents, in April 2010 the Indoor Tanning Association estimated that 25,000 businesses were providing indoor tanning services, including approximately 15,000 stand-alone tanning salons and approximately 10,000 other businesses that offer tanning services, such as spas, health clubs, and beauty salons." "The Congressional Joint Committee on Taxation estimated this tax would raise less than $50 million in the last 3 months of Fiscal Year 2010 and raise $200 million for Fiscal Year 2011."

But the tax hasn't raised nearly that much. Instead of 25,000 businesses filing, only about 10,000 have been filing. Not surprisingly, the tax is likely to raise less than $100 million in 2011, less than half of what was predicted.

I have never entered a tanning booth and hope never to do so. I can readily believe that if overused, they aren't great for your skin. But when the federal government starts trying to collect a small amounts of money from many small businesses, it's like an elephant standing on a ice rink trying to pick up peanuts. Sure, you get some peanuts. But the contortions and the effort seem hardly worth it. As you consider what the IRS has been going through to collect this tax, and the costs on businesses of record-keeping and dealing with the tax, remember that the $200 million that Congress hoped to raise with this tax represents about 1/20 of 1% of the $438 billion in total revenue-raisers in the health care reform bill. And consider the efforts needed to do this, laid out in dry detail in the TIGTA report:

Of course, the first step is to define which tanning services are covered and which are not: "This new excise tax applies to indoor tanning services paid for on or after July 1, 2010, and is 10 percent of the amount paid for the tanning services. Indoor tanning services are defined as services using ultraviolet lamps to induce skin tanning. There are other services provided by tanning salons that are excluded from the tanning tax. It does not apply to ‘spray’ tans or topical creams or lotions. In addition, it does not apply to phototherapy services performed by licensed medical professionals, during which individuals are exposed to light for the treatment of certain medical conditions. Tanning services are not taxable when provided by qualified physical fitness facilities (such as a workout facility or gym). The fitness facility must meet various tests to be exempt."

This line of business had not owed federal excises before. "[A]n IRS document describing compliance challenges states, “The tax is new and unusual for this industry, which has never experienced the imposition of a Federal excise tax on tanning services, and thus the overwhelming majority have never filed an excise tax return."

Thus, of course the IRS needed an an outreach program to let tanning booth owners know about the bill. This involved "Hosting live webinars and uploading videos on the YouTube web site," "Outreach to industry associations," "Contacting State licensing bureau," "Issuing electronic bulletins to tax professionals," and "Giving seminars at the Nationwide Tax Forums." For the IRS page with its Frequently Asked Questions about the tax, see here.

The new tax required reprogramming IRS computer systems. "There was a relatively short time period to prepare for receipt and processing of returns reporting the tanning tax. Accordingly, the IRS had to immediately update the computer systems used for processing tax returns. The IRS receives both paper and electronically transmitted returns. ... In general, the systems had to be updated to include a new abstract code for the tanning tax, which is a unique number assigned to each of the excise taxes."

And of course, now that only about half of those expected to pay are doing so, the IRS is needing to send thousands of follow-up letters, and then to follow up on those letters.

At the end of the day, the tanning tax probably collects more in revenue than the costs to the government and business of putting the tax into place and collecting it. But surely, the IRS resources could be better allocated (more audits on potentially large targets?). Indeed, given how little revenue the tanning tax corrects, it's probably misguided to think of it primarily as "tax" policy. It's some anonymous Congressman or staffer who doesn't like tanning booths sticking a tiny provision that almost no one hears about into an enormous bill. It's the sort of piddly annoying oddball regulation that gives the rest of government regulation a bad name.

Daron Acemoglu is amazingly wide-ranging, productive, and thought-provoking. A nice sample of his work and thinking emerges from a recently published interview with Douglas Clement of the Minneapolis Federal Reserve.

On the Dodd-Frank financial reform legislation

"I think the problem with the Dodd-Frank Act is that the amount of good it contains seems to be dwarfed by the amount of additional minute details it contains. That fails to achieve the intent of the regulation. It also gives better regulation a bad name, because people who are opposed to regulation can easily point to the page after page after page of paperwork and procedural things that Dodd-Frank wants you to do. And I am not convinced that the Dodd-Frank Act is going to prevent the next financial collapse if the financial system actually continues on its current trajectory. I don’t think anybody can claim that they know what’s going to happen in the next five years in the financial sector, but the financial sector has become more concentrated. It’s very profitable, it is still investing in highly risky assets and, in fact, it hasn’t really cleaned up its balance sheet to a great degree. The bonus culture, for example, was one of the elements that contributed to the crisis—not by any means the only one, or the most major one, but it was certainly an important factor. It has remained the same. And the Dodd-Frank Act doesn’t really do anything to deal with that. ...

I think something that’s much more effective—and again, I view it as a speed- bump-type of regulation—is to increase capital requirements. ... If you increase capital requirements, you’re essentially putting in speed bumps because the rate at which a bank can expand its balance sheet is going to be limited by the capital it has to a much greater extent than currently required. Those are the kinds of things that, as long as they’re not very detail-oriented, I think hold more promise. When they are detail-oriented, they are easier to overcome and thwart, and they are also much more costly to the daily functioning of banks."

On directed technical change and reducing carbon emissions

"Essentially, the bulk of the literature in environmental economics has been about how we have to tax economic activity to slow it down so that we don’t damage the environment. If you think of a single-sector economy, with one sector that depends on coal, or on gas, that’s the only thing you can do: slow down that one sector. If you want to reduce carbon emissions, you just have to slow down that sector. Now, you don’t directly slow it down; you change its composition of factors, perhaps, but you can’t let that sector take off at a very rapid rate and still, at the same time, limit carbon emissions.

Our perspective was, well, the economy has several technologies; some of them are cleaner than others. How should we shift toward the cleaner ones? When you look at the climate science, there’s a lot of emphasis precisely on this and on questions such as, When is it that nuclear power will become economical? When will geothermal or wind or solar solve both their cost and their delivery problems?

Therefore, the perspective shouldn’t be, How can we slow down economic activity? Instead, it should be, How can we shift the composition of economic activity away from dirty technologies to cleaner technologies? Now, that’s a very directed-technical-change-related question, but it already comes with a very important implication: The focus shouldn’t be on slowing down economic activity, but on changing its composition and changing the type of technological changes that the market generates.

Moreover, and importantly, we expect there to be a distinctive cumulative aspect to research. Different technologies often build on past successes in the same line of technology. So when you’re building a new car, you build on the past advances in car technology; you don’t as much build on advances in solar technology. In the same way as when you build new solar panels, you’re building on the previous solar panels, not on the diesel engine. What that means is that there’s going to be strong self-reinforcement in changing the direction of technological change. So when technological change shifts away from the dirty technologies that are so fossil-fuel-dependent to the cleaner technologies, it will also make it potentially cheaper to produce these innovations, these cleaner technologies, in the future."

On the relationship from political structures to economic growth

"But later in college and graduate school, I started working on issues related to human capital, economic growth and so on. But then after a while, I sort of realized, well, you know, the real problems of economic growth aren’t just that some countries are technologically innovative and some aren’t, and some countries have high savings rates and some don’t. They are really related to the fact that societies have chosen radically different ways of organizing themselves.

So there is much meaningful heterogeneity related to economic outcomes in the political structures of societies. And these tend to have different institutions regulating economic life and creating different incentives. And I started believing—and that’s reflected in my work—that you wouldn’t make enough progress on the problems of economic growth unless you started tackling these institutional foundations of growth at the same time."

Some applications to "Arab Spring"

"The big question is, Is this going to be a political revolution in the same way as the Glorious Revolution in England, which unleashed a fundamental process of transformation in the political system with associated economic changes? Ultimately, such political revolutions are fundamental to the growth of nations. That’s one of the arguments we make.

Or is it going to be the sort of revolution like the Bolshevik Revolution or the independence movements in much of sub-Saharan Africa in the 1960s, where there was a change in political power, but it went from one group to another, which then re-created the same system and started the same sort of exploitative process as the previous one?...

So, there is no guarantee that such movements will translate into a broad-based political revolution, as opposed to sort of a palace coup where one group takes control for another."

The U.S. economy has a major problem with unemployment, and in particular with unemployment of low-skilled workers. Apprenticeships are one major way that other countries, like Germany, have addressed this issue. Diane Auer Jones, a former former assistant secretary for postsecondary education at the Department of Education and now at something called the Career Education Corporation in Washington, DC, writes about this in the Summer 2011 issue of Issues in Science and Technology, in an article called "Apprenticeships Back to the Future."

One useful takeaway from the article is the contrast between how apprenticeship programs are a central element of education for the vast majority of students in places like Germany and Switzerland, while they are comparatively so minor in the U.S. labor market.

What apprenticeship programs are like in Germany and Switzerland

"In Germany and Switzerland, for example, apprenticeships are a critical part of the secondary education system, and most students complete an apprenticeship even if they plan to pursue postsecondary education in the future. It is not uncommon for German or Swiss postsecondary institutions to require students to complete an apprenticeship before enrolling in a tertiary education program. In this way, apprenticeships are an important part of the education continuum, including for engineers, nurses, teachers, finance workers, and myriad other professionals."

"An apprenticeship is a formal, on-the-job training program through which a novice learns a marketable craft, trade, or vocation under the guidance of a master practitioner. Most apprenticeships include some degree of theoretical classroom instruction in addition to hands-on practical experience. Classroom instruction can take place at the work site, on a college campus, or through online instruction in partnership with public- or private-sector colleges. Some apprenticeships are offered as one-year programs, though most span three to six years and require apprentices to spend at least 2,000 hours on the job. Apprentices are paid a wage for the time they spend learning in the workplace. Some apprenticeship sponsors also pay for time spent in class, whereas others do not. Some sponsors cover the costs associated with the classroom-based portion, whereas others require apprentices to pay tuition out of their wages. All of these details are part of the apprenticeship contract ..."

"In Switzerland, almost 70% of students between the ages of 16 and 19 participate in dual-enrollment vocational education and training (VET) programs, which require students to go to school for one to two days per week and spend the rest of their time in paid on-the-job training programs that last three to four years. ... Apprentices are subjected to regular assessments in the classroom and on the job, culminating in final exams associated with certification. In 2008, the completion rate for Swiss apprentices was 79%, and the exam pass rate among program completers was 91%. One of the main benefits of the Swiss apprenticeship system is that nearly 70% of all students participate in it, which means that students of all socioeconomic and ability levels are engaged in this form of learning. Such widespread involvement prevents the social stigmatization of apprenticeship programs, unlike in the United States where social prestige is almost exclusively preserved for college-based education and training. Moreover, because students entering dual-track VET programs are frequently high performers, they are academically indistinguishable from the students who elect university education rather than vocational training or dual education. As a result, Swiss dual-track VET students are likely to enter the workplace well prepared for work by possessing strong academic skills."

The status of apprenticeship programs in the United States

"In the United States, however, apprenticeships generally have been considered to be labor programs for training students to work in the skilled trades or crafts. They are not viewed as education programs, so they have not become a conventional part of most secondary or postsecondary systems or programs. ..."

"Apprenticeship programs do exist in the United States, but they are vastly underused, poorly coordinated, nonstandardized, and undervalued by students, parents, educators, and policymakers. The first successful federal legislative effort to promote and coordinate apprenticeships was the National Apprenticeship Act of 1937, commonly known as the Fitzgerald Act. This act treated apprentices not as students but as laborers, and it authorized the Department of Labor (DOL) to establish minimum standards to protect the health, safety, and general welfare of apprentice workers. The DOL still retains oversight responsibility through its Office of Apprenticeships, but the office receives an anemic annual appropriation of around $28 million."

"In each state, the DOL supports a state apprenticeship agency that certifies apprenticeship sponsors, issues certificates of completion to apprentices, monitors the safety and welfare of apprentices, and ensures that women and minorities are not victims of discriminatory practices. In 2007, the latest year for which data are available, there were approximately 28,000 Registered Apprenticeship programs involving approximately 465,000 apprentices. Most of the programs were in a handful of fields and industries, including construction and building trades, building maintenance, automobile mechanics, steamfitting, machinist, tool and dye, and child care."

Comment

In America, many schools and parents and students will speak out strongly in favor of strong commitments to "community service" and volunteer projects and unpaid short-term internships. But many of these same people tend to recoil if the discussion turns to devoting similar amounts of time to a paid apprenticeship. As an American, it's hard to imagine a Swiss-style system where 70% of students, spread across the distribution of incomes and education levels, are in apprenticeship programs. It's hard to think about apprenticeships that would spread across a much wider range of jobs and industries than we currently see in the U.S. Such a change would require a substantial adjustment from firms, existing employees, schools, government, and students themselves. But the current hand-off from the education system to the job market isn't going too well for a lot of Americans at a wide array of skill levels. Maybe apprenticeships could help.

The most recent World Development Report from the World Bank is centered on the theme: "Gender Equality and Development." The first chapter of the report focuses on gains that have been made, and I posted earlier today on surprising (to me) conclusion that around the world, gender equality has been largely attained in education and health. However, the second chapter focuses on dimensions of inequality that persist. The chapter focuses certain contexts where a high degree of gender inequality persists: for example, in lack of female participation in certain occupations and in political leadership, and in certain areas or economic groups where females are disadvantaged in many dimensions of life. But to me, the most appalling example of gender inequality is expressed by the problem of the "missing women." Based on evidence from biology and experience in high-income countries, we know that on average, slightly more men are born than women, and that women tend to have longer life-expectancies than men. But when we then apply those known proportions to certain countries and regions, we find that girls are missing at birth, and women are dying too frequently. Some excerpts, with footnotes and most references to tables and figures omitted, as usual:

Skewed sex ratios at birth and 3.9 million women missing under the age of 60

"First, the problem of skewed sex-ratios at birth in China and India (and in some countries in the Caucasus and the Western Balkans) remains unresolved (table 2.1). Population estimates suggest that an additional 1.4

million girls would have been born (mostly in China and India) if sex ratios at birth in these countries resembled those found worldwide. Second, compared with developed economies, the rate at which women die relative to men in low- and middle-income countries is higher in many regions of the world. Overall, missing girls at birth and excess female mortality under age 60 totaled an estimated 3.9 million women in 2008—85 percent of them were in China, India, and Sub-Saharan Africa."

A first main cause: Preference for Sons

"The disadvantage against unborn girls is widespread in many parts of Asia and in some countries in the Caucasus (such as Armenia and Azerbaijan), where the intersection of a preference for sons, declining fertility, and new technology increases the missing girls at birth. In China and India, sex ratios at birth point to a heavily skewed pattern in favor of boys. Where parents continue to favor sons over daughters, a gender bias in sex-selective abortions, female infanticide, and neglect is believed to account for millions of missing girls at birth. In 2008 alone, an estimated 1 million girls in China and 250,000 girls in India were missing at birth. The abuse of new technologies for sex-selective abortions—such as cheap mobile ultrasound

clinics—accounted for much of this shortfall, despite laws against such practices in many nations, such as India and China. Economic prosperity will continue to increase amniocentesis and ultrasound services throughout the developing world, possibly enabling the diffusion of sex-selective abortions where son-preferences exist. ... This does not imply that change is impossible: The Republic of Korea’s male-female sex ratio under age five was once the highest in Asia, but it peaked in the mid-1990s and then

reversed—a link to societal shifts in normative values stemming from industrialization and urbanization." A second main cause: Maternal Mortality

"The female disadvantage in mortality during the reproductive ages is in part driven by the risk of death in pregnancy and childbirth and associated long-term disabilities. Although maternal mortality ratios have fallen by 34 percent since 1990, they remain high in many parts of the world: Sub-Saharan Africa had the highest ratio in 2008 at 640 maternal deaths per 100,000 live births, followed by South Asia (280), Oceania (230), and Southeast Asia (160). Bangladesh, Cambodia, India, and Indonesia have maternal mortality ratios comparable to Sweden’s around 1900, and Afghanistan’s is similar to Sweden’s in the 17th century. ... Driving the high maternal mortality rates in many countries are poor obstetric health services and high fertility rates. Income growth and changes in household behavior alone appear insufficient to reduce maternal mortality; public investments are key to improving maternal health care services."

The most recent World Development Report from the World Bank is centered on the theme: "Gender Equality and Development." The first chapter of the report focuses on gains that have been made; the second chapter focuses on dimensions of inequality that persist. In this post, I'll focus on two patterns from the first chapter that I had not known about--on average, women the world around seem to have near-parity, and in some cases better than parity, with men in education and in health care. In a later post, I'll focus on what seems to me the most appalling widespread gender inequality that remains in the world today.

Global gender parity in education

"In the past decade, female enrollments have grown faster than male enrollments in the Middle East and North Africa, South Asia, and Sub-Saharan Africa. Gender parity has been reached in 117 of 173 countries with data (figure 1.1). Even in regions with the largest gender gaps—South Asia and Sub-Saharan Africa (particularly West Africa)—gains have been considerable. In 2008, in Sub-Saharan Africa, there were about 91 girls for every 100 boys in primary school, up from 85 girls in 1999; in South Asia, the ratio was 95 girls for every 100 boys.

"The patterns are similar in secondary education, with one notable difference. In roughly one-third of developing countries (45), girls outnumbered boys in secondary education in 2008 (see figure 1.1). Although the female gender gap tends to be higher in poorer countries, boys were in the minority in a wide range of nations including Bangladesh, Brazil, Honduras, Lesotho, Malaysia, Mongolia, and South Africa.

Tertiary enrollment growth is stronger for women than for men across the world. The number of male tertiary students globally more than quadrupled, from 17.7 million to 77.8 million between 1970 and 2008, but the number of female tertiary students rose more than sevenfold, from 10.8 million to 80.9 million, overtaking men. Female tertiary enrollment rates in 2008 lagged behind in only 36 developing countries of 96 with data (see figure 1.1). ...

"Although boys are more likely than girls to be enrolled in primary school, girls make better progress—lower repetition and lower dropout rates—than boys in all developing regions. ... Gender now explains very little of the remaining inequality in school enrollment ... In a large number of countries, a decomposition of school enrollments suggests that wealth is the constraining factor for most, and in only a very limited number will a narrow focus on gender (rather than poverty) reduce inequalities further ..."

Gender parity in health

"In most world regions, life expectancy for both men and women has consistently risen, with women on average living longer than men. The gap between male and female life expectancy, while still rising in some regions, stabilized in others. On average, life expectancy at birth for females in low-income countries rose from 48 years in 1960 to 69 years in 2008, and for males, from 46 years to 65. Mirroring the worldwide increase in life expectancy, every region except Sub-Saharan Africa added between 20 and 25 years

of life between 1960 and today. .... And since 1980, every region has had a female advantage

in life expectancy.

In most developing countries, fertility rates fell sharply in a fairly short period. These declines were much faster than earlier declines in today’s rich countries. In the United States, fertility rates fell gradually in the 1800s through 1940, increased during the baby boom, and then leveled off at just above replacement. In

India, fertility was high and stable through 1960 and then sharply declined from 6 births per woman to 2.3 by 2009. What took the United States more than 100 years took India 40 (figure 1.4). Similarly, in Morocco, the fertility rate fell from 4 children per woman to 2.5 between 1992 and 2004."

"On various other aspects of health status and health care, differences by sex are small. In many low-income countries, the proportion of children stunted, wasted, or underweight remains high, but girls are no worse off than boys. In fact, data from the Demographic and Health Surveys show that boys are at a slight disadvantage. ... Similarly, there is little evidence of systematic gender discrimination in the use of health services or in health spending. Out-of-pocket spending on health in the 1990s was higher for women than for men in Brazil, the Dominican Republic, Paraguay, and Peru. Evidence from South Africa reveals the same pro-female pattern, as does that for lower income countries. ... Evidence from India, Indonesia, and Kenya tells a similar story. ... For preventive health services such as vaccination, poverty rather than gender appears to be the major constraining factor ..."