From an economic point of view (and doubtless from other points of view, as well), the French present a puzzle. France is often perceived as having a government that practices heavy-handed intervention into the economy, sometimes known as dirigisme, but it is also obviously a high-income economy and has been a high-income economy for decades. So does this mean that France is less heavy-handed in economic interventionism than its reputation suggests? Or that the French have discovered an especially growth-friendly version of heavy-handed interventionism? How does France manage this balancing act?

Pierre Lemieux tackles this question in his essay "France: The end of the road, again?" in the Fall 2016 issue of

Regulation magazine (pp. 34-41). I was also reminded of an essay by

Olivier Blanchard, "The Economic Future of Europe," which often uses France as a specific example an appeared in the Fall 2004 issue of the

Journal of Economic Perspectives (where I have labored in the fields as Managing Editor since the first issue in 1987).

Both Lemieux and Blanchard point out that concerns about how the French government has a tendency to overcentralize its power and decision-making go back a long time. Lemieux points out that his was a theme of Tocqueville's back in 1856, in

The Ancient Regime and the French Revolution. He also mentioned that in 1970, French sociologist Michel Crozier published

The Stalled Society. In 1976, Alain Peyrefitte wrote

Le mal français (“the French disease”). Blanchard pointed out that in the year before his 2004 article, two books that made the estseller’s list in France were

La France qui tombe (

The fall of France), by Nicolas Baverezm and

Le desarroi Francais (T

he French disarray), by Alain Duhamel. Lemieus refers to a book published last year by Gilbert Cette and Jacques Barthélémy published

Réformer le droit du travail (Reform the Labor Code).

As a starting point, here's some evidence on the higher degree of regulation in the French economy. Lemieux notes: "Public expenditures amount to 57% of French gross domestic product, the fourth-highest percentage in the OECD, after Greece, Slovenia, and Finland. This compares to 45% for the OECD unweighted average and 39% for the United States." In measures of "economic freedom" for the countries of the world, the US tends to rank around 10th, while France tends to rank around 70th.

However, Lemieux also offers some evidence on the other side: "Not all industries are more regulated in France than in America. The OECD’s Services Trade Restrictiveness index shows France as less regulated than the United States in commercial banking, insurance, broadcasting, and many modes of transport. Even the labor market is less regulated in France with regard to many trades and professions. In the United States, nearly 30% of jobs require a license." Moreover, France (like many other economies) has gradually been moving in the direction of less regulation.

But the area of labor market rules, in particular, is one where France stands out as especially heavy-handed. For example,

although only about 8% of French workers are officially union members, 98% of French workers are covered by collective bargaining. Lemieux writes:

"[A]ny firm of more than 49 employees must create a “work council” (comité d’entreprise) chaired by a representative of the owners but composed of trade union representatives and representatives elected directly by the employees. Consultation of the work council is compulsory on many business decisions. Even businesses of 11–49 employees are forced to allow the election of employee representatives. To appreciate the spirit of the 2,880-page labor Code, consider that the French government is currently pushing businesses to negotiate with their workers’ representatives a “right to disconnect,” referring to after-hours work-related electronic communications. The Department of labor, Employment, Occupational Training, and Social Dialogue (why they didn’t add “General Happiness” to the name is a mystery) explains that “the employees of a large firm are not obliged to answer emails outside of office hours.”

As another example, here's a figure about "employment protection" from

2015 OECD Economic Survey of France--basically, how hard it is for a firm to fire or lay off workers. The figure shows the US and Canada off on the far left, with little employment protection, while France is off near the far right.

Lemieux notes: "Because of the cost of firing employees, firms are incited to resort to short-term labor contracts, a loophole that further regulations have tried to limit. In France, a short-term contract may not extend beyond 24 months. The employed work force has thus acquired a dual structure: on one side, the “insiders”—regular workers protected against dismissal; on the other side, the “outsiders,” who survive on short-term contracts and hop fromjob to job. Outsiders make up about 15% of the employed, a proportion that climbs over 50% in the 15–24 age category."

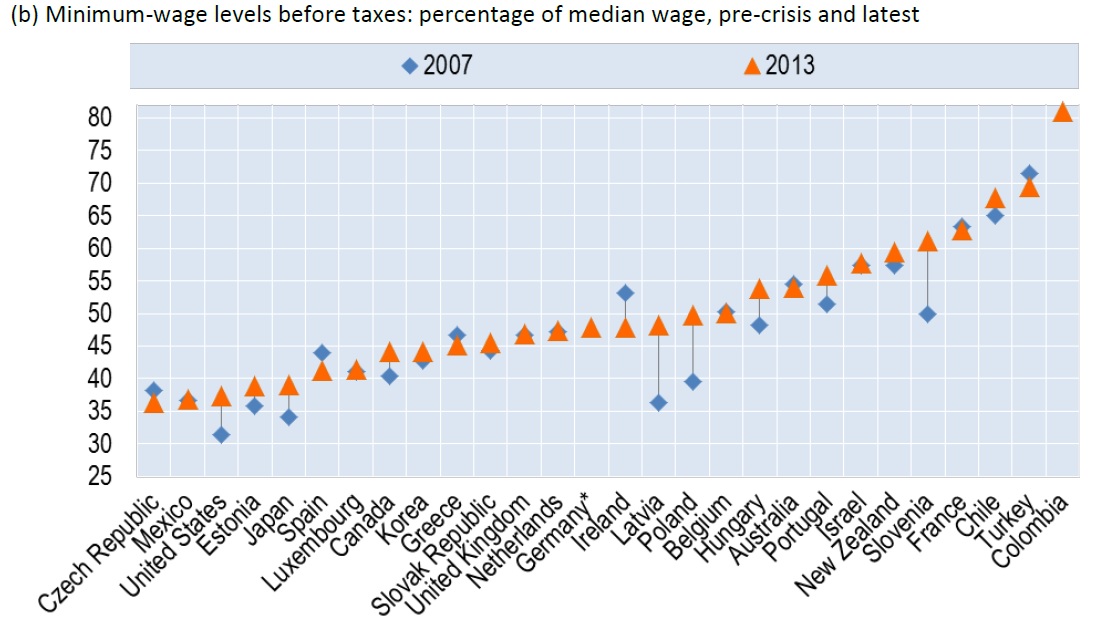

The minimum wage in France is also comparatively high compared to other countries. Here's a figure from a

a 2015 OECD report on minimum wages, which shows minimum wages as a percentage of the median wage in the country. Again, the US is off on the left, with a minimum wage about 35% of the US median wage, while France is off near the right, with a minimum wage at about 60% of the median wage.

Here's the unemployment rate in France during the last couple of decades, from the

Trading Economics.com website. It seemed for a time in the early 2000s as if France was making some progress on its unemployment rate issues, even if the unemployment rate had only fallen to a still-unsatisfactory 7.5%. But now the unemployment rate is back up around 10% again, and has been there for three years. For comparison, remember that in the aftermath of the Great Recession, the US unemployment rate peaked at 10% in October 2009, before starting a long glide down to the current rate of 5%. Try to imagine the political turmoil in the US if the unemployment rate was higher now, seven years after 2009. That's the situation in France.

If you focus only on the youth unemployment rate in France, it's been roughly at 24-26% since 2009. Of course, France's labor market regulations aren't the only cause of unemployment and lower labor force participation in France, the generally torpid European economy bears a large share of the blame. But the many labor market regulations aren't helping, either.

The result of these labor market regulations is that France is running a high-powered modern economy for many of those who have jobs, but with high unemployment or temporary work for many others. Blanchard offered an interesting summary of the situation in his 2004 JEP essay. The table shows that when looking at GDP per capita, France went a little backward compared to the US from 1970 to 2000. However, if one looks at GDP per hour worked during this time, France caught up to the US level, while if one looks at hours worked per capita, France started at above the US level in 1970 but then declined to 71% of the US level by 2000.

In short, the French are very productive during their working hours. But the French now work many fewer hours per capita, in part because the labor force participation rate (the share of adults either employed or looking for work) is lower in France, in part because of continuing high unemployment rates, and in part because a number of jobs have more vacation per year than is common in the US.

A couple of warnings about those high rates of productivity in France should be noted. One is that in the US, lower-wage and lower-productivity worker are more likely to have jobs than in France. As a result, France's higher productivity is in part because a substantial share of those who would tend be the lower-productivity workers (like young workers, for example) just aren't working at all.

The other concern is that productivity in France has in fact started to lag, starting in the mid-1990s, especially if one looks at "multifactor" productivity, which doesn't just divide output by hours worked, but also adjusts for other inputs like capital investment. Blanchard had raised this possibility in his 2004 essay, noting that while the evidence at the time of his writing was not yet decisive, "most observers now believe that we have indeed seen a

change in relative trends [of productivity growth in the US and continental Europe], starting around 1995." Lemieux cites other evidence and writes:

"Since the mid-1990s, France and many other European countries

(but not the UK) have suffered a widening gap with the U.S.

standard of living. During that period, the culprit was the slowdown

of multifactor productivity growth, especially noticeable

in France. According to another paper by Cette and Lopez, the

underlying causes were a slower diffusion of the new information

technologies, structural rigidities in labor and product markets,

and a less educated working population. From 1995 to 2012,

French GDP per capita grew at a meager 1% per year."

None of this discussion should be read as a prediction of doom for the French economy, which seems certain to remain a high-income economy. But it does suggest that French dirigisme is not cost-free: specifically, the costs in the last couple of decades are measured in elevated unemployment, lower labor force participation rates, a larger number of temporary jobs, and sluggish growth in productivity and the standard of living.