Each summer for the last 20 years or so, I've spent a few days at theStanford Summer Economics Institute for High School Teachers, giving some of the lectures and talking pedagogy with the participants. This year, one of my talks was on "The Economics of Immigration." Here are some of my favorite Powerpoint slides from the presentation (as always in a jpeg format so they are easy to copy for your own presentation, if you wish), along with a few thoughts.

Immigration--legal and illegal combined--is often measured by looking at the share of the U.S. population that is foreign-born, which is available through Census data. America's previous huge wave of immigration took the foreign-born share of the population up to around 14% for the later decades of the 19th century and the early 20th century. As the figure shows, the wave of immigration in recent decades hasn't topped that level yet, but is near 12% of population. It's worth remembering that America has long fluctuated between two views of immigration: one view represented by "give me your tired, your poor" written beside the Statue of Liberty, and the other represented by fierce restrictions on immigration, like effective ban on immigration from China starting in the 1880s, or the strict and limited quotas on immigration imposed in the 1920s. Both welcoming and opposing immigration are as American as apple pie.

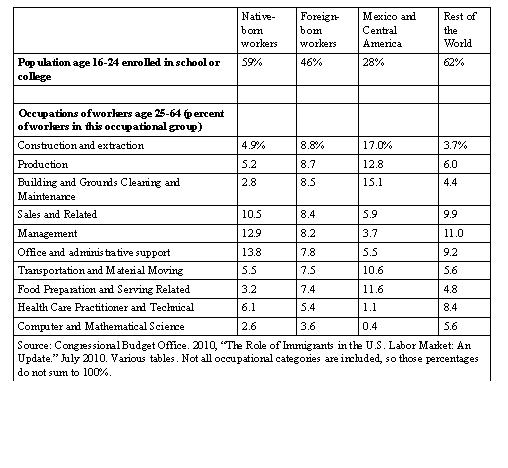

The current wave of immigration is somewhat split by skill level. Immigrants from Mexico and central America typically have an education level considerably below the American average. However, immigrants from other regions of the world have an education level above the American average. The tables, based on data from a Congressional Budget Office Report in July 2010, also show that this difference is manifested in the sorts of jobs that migrants take. The relatively low-skilled immigrants from Mexico and Central America are more likely to end up in jobs like construction, building and grounds maintenance, and food preparation and service. The relatively high-skilled immigrants from the rest of the world are more likely to end up in jobs like health care practitioners, mathematics, or computer science.

The question of how much immigration affects wages of U.S. workers is highly controversial. The answer often seems to depend on whether one analyzes data from a cross-section of cities, which tends to find that more immigration helps wages of native-born workers of all skills, or if one analyzes a time series of immigration patterns over time, which often finds that immigration hurts the wages of low-skilled native-born workers. Another factor underlying these different answers are analysis of whether low-skill immigrant labor is a complement or a substitute for low-skill native-born labor. The figure contrasts findings from two studies with different approaches. It is intriguing that even the studies which find a negative effect of immigrants on the wages of some skill levels of native-born labor find an effect that is quite small--no more than a few percentage points.

Finally, U.S. immigration policy is distinguished from most other countries both by the large numbers it admits, and also by its emphasis on handing out immigration slots based on family ties, rather than for work-related reasons. Here's a table from the Federal Reserve Bank of Dallas, based on OECD data, showing the difference. A group of experts convened in 2009 by the Brookings Institutions and the Kenen Institute for Ethics at Duke University estimated that if family preferences in immigration law were limited to spouses and children, and not extended to aunts, uncles, cousins, and the like, this change could free up 160,000 slots to be filled by skill-related immigrants. This change would roughly double the level of skill-related U.S. immigration.

Note: In an earlier version of this post, there was a typo in the second paragraph, where I referred to "12% of GDP" instead of "12% of population." This version incorporates the correction. Thanks to sharp-eyed reader T.D. for calling this to my attention.

I confess that since the federal funds interest rate fell to near-zero in late 2008, I haven't paid much attention to it. But Todd Clark and John Lindner of the Cleveland Fed (pp. 5-7) offer a quick overview of some factors that have affected that rate since late 2010. In particular, they discuss a change I probably should have known about, but had not: apparently, the Federal Deposit Insurance Corporation no longer uses bank deposits as the base for deposit insurance premiums, but now uses the difference between bank assets and bank equity as the base for deposit insurance.

Clark and Lindner write: "Historically, the federal funds rate has been the primary instrument of monetary policy. Daily federal funds rates since November 2010 fall loosely into a series of three trends, all of which can at least be partially explained by an event that has influenced market participants. In November, the Fed announced the second round of large-scale asset purchases, which consisted of the Fed buying $600 billion in Treasury securities through the end of June 2011. From early November there was a steady decline in the federal funds rate from about 20 basis points to 17 basis points. The purchases increased the supply of reserves in the federal funds market, which pushed down the price, the federal funds rate. Put another way, the increased supply forced cash investors to compete in the market at lower interest rates."

"Similarly, the decision by the Treasury in early February 2011 to wind down its Supplemental Financing

Account balance inserted more reserves into the market for cash investors to place. Combined with the asset purchases, this move accelerated the decline in the federal funds rate. This acceleration was reflected in another 4 basis point decline, from 17 basis points to 13 basis points, over the following two months."

"By far the most studied of the three events, however, has been the change in the FDIC assessment base for deposit insurance. Many observers have argued that this is the move that caused the dramatic

drop in the federal funds rate at the beginning of April, and it has also been credited for holding the

eff ective rate at a fairly constant level of 10 basis points."

"With the new FDIC assessment policy, insured depository institutions will be charged an insurance premium not on their amount of deposits, but on the difference between their total assets and their equity. Broadly speaking, this equates to their liabilities, but there are some subtleties that we are going to skip over. Due to the change in the assessment base, depository institutions are now forced to pay an extra fee for any financed assets, including funds that they might borrow in the federal funds market. Since many of the funds available in the federal funds market are provided by nonbank institutions, the current primary purpose of borrowing these funds is to earn the interest on reserves (IOR) available at the Fed. So, banks are making the diff erence in the two rates (fed funds and IOR) as a profit. The new assessment implicitly increases the cost of the federal funds by adding that assessment rate onto the fed funds rate. As a result, some banks have exited the market, reducing overall demand for the funds dramatically. The fall in demand has reduced the funds rate."

In a previous post, I passed along some of the comments that the IMF had to make about U.S. fiscal policy and how and when to reduce budget deficits in the annual IMF report on the U.S. economy. Here, I'll look at an intriguing comparison that the IMF offers between the aftermath of the Great Recession and the previous nine U.S. business cycles. In particular, there is a considerable disjunction in the current recovery between a lot of the output and employment statistics, which look quite bad, and the health of the business and financial sector, which looks quite good.

In the table that follows, the last ten U.S. business cycles in reverse chronological order, with the most recent at the top, are the rows. The columns offer a list of various economic factors. Instead of a bunch of numbers, the statistics were ranked for each of the 10 recoveries, and then portrayed in this way: dark green means the strongest two recoveries in this category; light green means the 3rd and 4th strongest recoveries in this category; white means the 5th and 6th strongest recoveries; light red means the 7th and 8red strongest recoveries out of these ten; and dark red means the weakest two recoveries in each category.

By far the most striking pattern in the table is that the current recovery has a lot of red shading on the left, but a lot of green shading on the right. That is, the current recovery looks pretty bad compared with its predecessors on GDP, consumption, personal income, jobs, and unemployment. But it looks pretty good compared with its predecessors on financial and nonfinancial corporate profits, manufacturing orders, stock prices, and the health of banks. How can these factors be reconciled?

Part of the answer lies in the good picture for U.S exports, which are helping to drive manufacturing orders, production of equipment and software, and nonfinancial corporate profits. Part of the answer must be that after several years of making sure that the financial sector has easy access to cheap credit, banks are much better off than a few years ago.

But the disjunction remains. Firms have profits, but haven't yet started hiring. Banks and other financial institutions have become much healthier, but in many areas haven't significantly boosted their lending. It's as if many U.S. financial and nonfinancial companies are all holding their breath, waiting for some high-pitched dog whistle that only they can hear before hiring and lending picks up.

"Fiscal policy. Consolidation needs to proceed as debt dynamics are unsustainable and losing fiscal credibility would be extremely damaging. However, the pace and composition of adjustment should be attuned to the cycle. A politically-backed medium-term framework that raises revenues and addresses long-term expenditure pressures should be the cornerstone of fiscal stabilization. The official deficit reduction proposals could be too front-loaded given the cyclical weakness and, at the same time, insufficient to stabilize the debt by mid-decade." (p. 1)

"Unfavorable fiscal outcomes. These could take the form of a sudden increase in interest rates and/or a sovereign downgrade if an agreement on medium term consolidation does not materialize or the debt ceiling is not raised soon enough. These risks would also have significant global repercussions, given the

central role of U.S. Treasury bonds in world financial markets. At the opposite extreme, an excessively large upfront fiscal adjustment could significantly weaken domestic demand ..." (p. 11)

"Short-term U.S. spillovers on growth abroad are uniquely large, mainly reflecting the pivotal role of U.S. markets in global asset price discovery. While U.S. trade is important, outside of close neighbors it is the global bellwether nature of U.S. bond and equity markets that generates the majority of spillovers." (p. 13)

"The authorities have a number of options to achieve fiscal sustainability without large negative short term effects on activity. Social Security reform would help reduce long-term fiscal imbalances without undermining the ongoing recovery—measures such as increasing the retirement age while indexing it to longevity and trimming future benefits for upper-income retirees would have a minimal impact on current private spending. Identifying additional saving in health care and other mandatory spending categories would also be highly desirable, including through greater cost sharing with the beneficiaries, curbs to the tax exemption for employer-provided health care, and targeted savings identified by the President’s Fiscal Commission. Meanwhile, the tax system is riddled with loopholes and deductions worth over 7 percent of GDP. Gradually reducing these tax expenditures (including eventually the mortgage interest deduction which largely benefits upper-income taxpayers) would help raise needed revenue while enhancing efficiency. In the

longer term, consideration could also be given to introducing a national VAT or sales tax, as well as carbon

taxes."

I would like to take this opportunity to heartily endorse Association 3E: Ethics, Excellence, Economics.

I discovered this organization last weekend, when my wife and I were having a 20th anniversary child-free getaway weekend in the Napa Valley. While working my way through the tasting plates at the Wine Spectator Greystone Restaurant run by the Culinary Institute of America restaurant, I discovered: "The mission of Association 3E is the advancement of excellence in extra virgin olive oil." Yes, Ethics, Excellence, Economics is the slogan for a group of producers of super-premium olive oils. I lay no claim to a sophisticated palate for super-premium olive oils. My unsophisticated, seat-of-the-pants opinion is YUM.

Zogby writes: "In an interactive poll taken immediately after Obama’s 2008 election, 68% of adults said it is possible for them and their families to achieve the American Dream, and 18% said it did not exist. Almost as many (62%) agreed most middle class families could achieve it. Our poll taken a week ago showed 49.7% believing the dream was achievable for their families, 30% saying it did not exist and 44% agreeing it is achievable for most middle class families. ... There was little change over three years in how people defined the American Dream. In 2008, 38% defined it as material goods and 43% said it was spiritual happiness. Now, 40% choose the material and 37% spiritual. Above I suggested our loss of national confidence is about more than just economic well-being. The reason is our finding that those who define the American Dream as material are only slightly more likely to say it doesn’t exist than are those who define it as spiritual happiness. It seems we have both an economic and psychological recession."

But just what is the "American Dream"? The phrase “the American Dream” was coined by a Pulitzer prize-winning historian named James Truslow Adams in his 1931 book The Epic of America. Truslow described the American Dream in this way (pp. 415-416):

"But there has been also the American dream, that dream of a land in which life should be better and richer and fuller for every man, with opportunity for each according to his ability or achievement. It is a difficult dream for the European upper classes to interpret adequately, and too many of us ourselves have grown weary and mistrustful of it. It is not a dream of motor cars and high wages merely, but a dream of social order in which each man and each woman shall be able to attain to the fullest stature of which they are innately capable, and be recognized by others for what they are, regardless of the fortuitous circumstances of birth or position. I once had an intelligent young Frenchman as a guest in New York, and after a few days I asked him what struck him most among his new impressions. Without hesitation he replied, "The way that everyone of every sort looks you right in the eye, without a thought if inequality. Some time ago a foreigner who used to do some work for me, and who had picked up a very fair education, occasionally sat and chatted with me in my study after I had finished my work. One day he said that such a relationship was the great difference between America and his homeland. There, he said, "I would do my work and might get a pleasant word, but I could never sit and talk like this. There is a difference there between social grades which cannot be got over. I would not talk to you there as man to man, but as my employer.""

"No, the American dream that has lured tens of millions of all nations to our shores in the past century has not been a dream of merely material plenty, though that has doubtless counted heavily. It has been much more than that. It has been a dream of being able to grow to fullest development as man and woman, unhampered by the barriers which had slowly been erected by older civilizations, unrepressed by social orders which had developed for the benefit of classes rather than just for the simple human being of any and every class. And that dream has been realized more fully in actual life here than anywhere else, though very imperfectly even among ourselves."

Adams puts this idea of the "American dream" at the center of his description of telling the American narrative and describing what it means to be an American (p. 174):

"If Americanism in the above sense has been a dream, it has also been one of the great realities of American life. It has been a moving force as truly as wheat or gold. It is all that has distinguished American from a mere quantitative comparison in wealth or art or letters or power with the nations of old Europe. It is Americanism, and its shrine has been in the heart of the common man. He may not have done much for American culture in its narrower sense, but in its wider meaning it is he who almost alone has fought to hold fast to the American dream. This is what has made the common man a great figure in the American drama. This is the dominant motif in the American epic."

The Zogby poll tells us that more people are feeling discouraged in July 2011 than in November 2008, which isn't an enormous shock given the Great Recession and the Long Slump that has followed. I'm dubious that the survey tells us much about the "American dream" in the broader sense of James Truslow Adams, which includes material well-being and personal happiness, but also includes some broader issues: opportunity to shape one's destiny; when social order means less and individuals mean more; when social equality is a common presumption in a way that reaches beyond equal treatment before the law; and when the successes and failures of the country are judged by how they affect everyday people.

McKinsey estimates that the U.S. economy needs 21 million additional jobs by 2020 if the U.S. economy is to have full employment that year. It argues that this goal is achievable if "high-job-growth scenarios" are met in six sectors: "health care, business services, leisure and hospitality, construction, manufacturing, and retail. These sectors span a wide range of job types, skills, and growth dynamics. They account for 66 percent of employment today, and we project that they will account for up to 8 percent of new jobs created through the end of the decade."

What do these high-job-growth scenarios look like in each sector? Here are some comments from the McKinsey report, along with some of my own reactions. I also draw on some projections from the Bureau of Labor Statistics, published in the November 2009 Monthly Labor Review, predicting the "Occupations with the largest job growth" from 2008 to 2018. I'll say up front that while I'm an admirer of both the BLS and the McKinsey Global Institute, projecting which kinds of jobs will grow in the future is a very uncertain business.

Forecasting the future is hard. But it can still be a useful tool for thinking about the future evolution of the U.S. economy.

Health care

McKinsey writes: "The health care sector has been the most reliable engine of job growth in the economy over the past decade, adding jobs even during the recession. Moreover, 71 percent of those employed in the sector have more than a high school education, compared with 62 percent economy-wide, and average wages are 10 percent higher than the national average for service-sector jobs. ... Although one-third of health care jobs are in hospitals, the largest job growth over the past decade has been in nursing and residential care, social assistance, and home health care services." As McKinsey goes on to point out, with an aging population and expanding insurance coverage, more jobs in this area seem likely.

This makes a lot of sense to me. In the BLS projections, four of the top nine occupations for job growth are in this area: Registered nurses (#1), Home health aides (#2), Personal and home care aides (#5) and Nursing aides, orderlies, and attendants (#9). But a couple of reactions seem worth noting here.

First, the "health care jobs" are tending to move away from doctors in hospitals, and toward aides that help at home. I suspect that this trend will continue. A huge share of illness and health care costs are caused by chronic conditions. As the Centers for Disease Control puts it: "Chronic diseases—such as heart disease, cancer, and diabetes—are the leading causes of death and disability in the United States. Chronic diseases account for 70% of all deaths in the U.S., which is 1.7 million each year. These diseases also cause major limitations in daily living for almost 1 out of 10 Americans ...." Many chronic diseases share the general property that if they are well-managed every single day, with a combination of drugs, lifestyle, and certain kinds of monitoring of physical conditions, it is possible to reduce the need for enormously costly episodes of hospitalization. Using a mixture of information and communications technology, hooked into medical technology that can be used in the home and personal reminders when needed, seems like a possible win-win-win scenario in term of improving health, reducing health care costs, and developing a new type of industry.

"For every office-based physician in the United States, there are 2.2 administrative workers. That exceeds the number of nurses, clinical assistants, and technical staff put together. One large physician group in the United States estimates that it spends 12 percent of revenue collected just collecting revenue. Canada, by contrast, has only half as many administrative workers per office based physician. The situation is no better in hospitals. In the United States, there are 1.5 administrative personnel per hospital bed, compared to 1.1 in Canada. Duke University Hospital, for example, has 900 hospital beds and 1,300 billing clerks. On top of this are the administrative workers in health insurance. Health insurance administration is 12 percent of premiums in the United States and less than half that in Canada. International comparisons of medical care occupations are difficult, but they suggest that the United States has more administrative personnel than other

countries do. Data from the Luxembourg Income Study indicate that the United States has 25 percent more healthcare administrators than the United Kingdom, 165 percent more than the Netherlands, and 215 percent more than Germany."

In short, vastly improved use and coordination of information technology in U.S. health care, which is desirable on a number of grounds like better coordination of care across providers, would also trim a large number of jobs in the U.S. health care system.

Business services

McKinsey writes: "Nearly 17 million Americans are employed in business services, making it second only to the government sector in terms of total employment. ... [E]mployment growth in the sector was essentially flat for the 2000-2010 decade ... Business services include occupations ranging from administrative assistants and janitors to architects and research scientists. The vast majority of jobs fall into two broad subsectors of roughly 7.5 million each: administrative services, and professional, scientific, and technical services ..."

Three of the top eight job growth categories for 2018, according to the BLS, fall into this category:

Customer service representatives (#3), Office clerks, general (#7), and "Accountants and auditors (#8).

However, McKinsey's high-job-growth scenario here depends on a pattern in which U.S. companies decide to do less offshoring of service jobs, and even move some back to the United States. "In our interviews, companies say they are considering moving service jobs back to the United States, citing concerns over quality, reliability, high turnover, and rising wages abroad .." Fair enough. I've read about cases where outsourcing didn't work well, too. But on the other side, I suspect that many possible ways of outsourcing business services jobs are only just being discovered. I'm dubious of a scenario where the U.S. brings home more jobs than it increases outsourcing.

Leisure and Hospitality

McKinsey writes: "[T]o reach the high-job-growth scenario, the United States needs to retake lost ground in global tourism. While international long-haul travel increased by 31 percent from 2000 to 2009, the number of visitors to the United States dropped. Foreign visits fell from 26 million in 2000 to 18 million in 2003, before recovering to 24 million in 2009. ... In particular, the United States is not getting its share of tourism from a rising global middle class. More Chinese tourists visit France than the United States, for example. A weak dollar should help bring in tourists from China, Brazil, India, and other fast-growing economies ..."

By some measures, if one combines both both international and domestic tourism, tourism is the largest industry in the world. Many Americans tend to think of this country as a point of departure for U.S. tourists going elsewhere, not as a destination for the rest of the world. But in a globalizing world, with a rapidly expanding global middle class, we need to rethink the economic importance of tourism.Of course, international tourism is entangled with concerns about preventing terrorism; restrictions on tourism after 9/11 are a major reason for the drop in U.S. tourism from 2000 to 2003. But having people from around the world visit the U.S. is also one of the most powerful steps the United States can take to dispelling myths about this country and to showing how a free and open society functions. Expanding tourism strikes me as both an economic goal, and also an important part of America's broader international relations agenda.

Without tourism, this is a fairly low wage area of jobs in areas like food service. According to BLS,

"Combined food preparation and serving workers, including fast food" will be the fourth-largest job growth category from 2008 to 2018.

Construction

McKinsey's high-job-growth scenario here relies on housing starts returning to their long-term average by about 2014, on additional government incentives for energy efficiency retrofitting, and on expanded infrastructure spending. The BLS lists "Construction laborers" 11th among job categories with largest growth from 2008 to 2018. This particular scenario doesn't seem all that likely to me. Given very tight government budgets, I don't think we're going to see a wave of infrastructure spending, nor substantial government incentives for energy retrofitting. I'm not confident that home-building will be resurrected three years from now.

Manufacturing

McKinsey's The high-job growth scenario here is that if a low dollar encourages exports, and if some of the trend to outsourcing is reversed, then "we can envision a scenario in which manufacturing job losses are much smaller or even stop in the decade ahead." This seems to me a fair statement of the optimistic view on manufacturing jobs, but it's hard to see a lot of reason for optimism.

There were about 18 million manufacturing jobs in the U.S. in the late 1960s. By the late 1970s, this had climbed to 19.4 million. But manufacturing jobs had dropped to 17.2 million by 2000, before plummetting to

fewer than 12 million in 2009 and 2010. Perhaps a modest bounce-back will occur, but it's hard for me to be more optimistic than that.

Retail

This high-job-growth scenario here is based on a revival of consumer spending as the Long Slump of the U.S. economy gradually turns into more of a real recovery. The BLS ranked "Retail salespersons" sixth among occupations for job growth from 2008 to 2018.

To me, the future of retail seems very muddled in world where can buy everything from books to a lawn mower to groceries on Amazon, along with any other number of on-line sellers. Businesses are still figuring out how best to integrate bricks-and-clicks, that is, the desire of many consumers to see and touch and talk about many objects before purchasing them, together with the efficiencies of ordering on-line and delivering from a warehouse. I'm not at all sure how this will work out, but my suspicion is that there may end up being more new jobs in the process of delivering goods from warehouses to people's homes, or to a set of as-yet-undetermined safe locations near people's homes, than additional jobs in conventional retail positions.

What are other possible options for creating jobs?

So that's the McKinsey list. What else is there? In particular, it's intriguing to brainstorm about certain kinds of jobs that are not extremely high on skills (not everyone is going to be a research scientist), but also aren't extreme low-wage jobs either. These would be jobs where people learn and develop skills and experience, and perhaps where they can leverage their skills by interacting with information and communications technology. In addition, they should be jobs that can't easily be outsourced, maybe because geographically tied to U.S. (like provision of support for chronic health conditions) or maybe because it is not the kind of routinized task where outsourcing works well.

Along with some of my suggestions above, here are three possibilities:

1) Jobs in energy production. I don't mean green energy here, which will depend on government subsidies for awhile yet, but rather exploiting oil and natural gas that is now available through technologies like fracking. Of course, there is a political dimension as to how fast this might proceed, or whether it will proceed at all. But there are significant number of fairly well-paid jobs in this industry--as North Dakota is already illustrating.

2) Consumer technology services. Many consumers have lives that are ever-more-full of interlocking technologies. Most of us are happy to use these technologies, but we have little intrinsic interest in hooking them up or debugging them when they go awry. Along with plumbers and carpenters and electricians, the "home repair" category may come to include people who can set up, interconnect, and do at least basis repairs on your gear.

3) The next big technology breakthrough. In the last few decades, productivity growth has been built in large part on the technological gains in information and communications technology, and in finding ways to apply those gains across the economy. This branch of technology growth still has a way to run, but it's worth thinking about what might come next. Materials science? Biotechnology? Nanotechnology? The key is to have a technology that makes continuing and rapid gains for a long period of time, in the way that electronics has done.

My crystal ball for predicting future job growth is all clouded up. Other suggestions welcome. The U.S. economy needs them.

Start with the G-7 countries: that is, the United States, Japan, Germany, France, Italy, United Kingdom, and Canada. Now compare them with the largest 7 "emerging" economies: the E-7 would beChina, India, Brazil, Russia, Indonesia, Mexico and Turkey. A January 2011 report from pwc offers some projections comparing where these two groups are headed by 2050.

First, compare the total size of the G-7 and the E-7 economies, in 2009. At market exchange rates, the E-7 is about one-third of the G-7 in 2009. In purchasing power parity exchange rates (which help to account for the fact that money can often buy more of certain goods in low-income countries), the E-7 is about two-thirds of the G-7 in 2009. "In our base case projections, the E7 economies will by 2050 be around 64% larger than the current G7 when measured in dollar terms at market exchange rates (MER), or around twice as large in PPP terms."

This change represents a remarkable shuffling of the economies of the world. To get a sense of the change, compare the rank order of the economies of the world in 2009 and 2050. In 2009, the U.S. is the world's largest economy. By 2050, U.S. economy will be about 2.5 times as large--and is projected to be in third place in absolute size, behind China andIndia. What other countries move up the rankings notably by 2050? Brazil, Mexico, Indonesia, Turkey, Nigeria, and Vietnam. To my 20th century mindset, some of those countries just don't seem like global economic heavyweights. Time to start adjusting my mind to the coming realities.

Of course, per capita GDP looks quite a bit different. China and India have vastly larger populations than the United States. After 40 more years of rapid growth, per capita GDP in China will by 2050 roughly reach the U.S. per capita GDP in 2009. But by that time, U.S. per capita GDP will have more-or-less doubled. On a per capita GDP basis, China won't come close to catching any of the G-7 countries even by 2050--in fact, on these projections, China doesn't catch up to Mexico in per capita GDP by 2050.

Shane Frederick wrote a nice short article in the January-February 2011 issue of the Harvard Business Review on "The Persuasive Power of Opportunity Costs." He points out that framing choices by making opportunity costs explicit can persuade people to make certain choice--especially because the opportunity costs can be chosen to appear large or small. Opportunity cost, of course, is one of the first concepts taught in any intro economics course.

Here's an example from Frederick where the explicit opportunity cost appears large:

"While shopping for my first stereo, I spent an hour debating between a $1,000 Pioneer and a $700 Sony. Perhaps fearing that my indecision would cost him a sale, the salesman intervened with the comment "Well, think of it this way--would you rather have the Pioneer, or the Sony and $300 worth of CDs?"

Wow. The Sony--and by a large margin. Twenty new CDs were too great a sacrifice for the slightly more attractive Pioneer. Although I could subtract $700 from $1,000 and was capable--in principle--of recognizing that $300 could be used to buy $300 worth of CDs, I hadn't considered that until the salesman pointed it out."

Here's an example from Frederick where the opportunity cost is framed to sound small:

"[Here's a] strategy for those offering expensive products or policies: Cast the opportunities given up as something unattractive or unimportant. An ad by De Beers did this brilliantly. It depicted two large diamond earrings with the tagline "Redo the kitchen next year." Clever. It implied that the cost of the diamonds was merely a slight delay in a renovation. In fact, if a consumer spent the money reserved for the kitchen on the diamonds, it might take him or her much more than a year to save that amount again."

And here's a political example of making opportunity costs explicit, from the 1953 "Chance for Peace" speech given by President Dwight Eisenhower, who said:

"The cost of one modern heavy bomber is this: a modern brick school in more than 30 cities.…We pay for a single fighter with a half million bushels of wheat. We pay for a single destroyer with new homes that could have housed more than 8,000 people."

"Jan Pen, a Dutch economist who died last year, came up with a striking way to picture inequality. Imagine people’s height being proportional to their income, so that someone with an average income is of average height. Now imagine that the entire adult population of America is walking past you in a single hour, in ascending order of income."

"The first passers-by, the owners of loss-making businesses, are invisible: their heads are below ground. Then come the jobless and the working poor, who are midgets. After half an hour the strollers are still only waist-high, since America’s median income is only half the mean. It takes nearly 45 minutes before normal-sized people appear. But then, in the final minutes, giants thunder by. With six minutes to go they are 12 feet tall. When the 400 highest earners walk by, right at the end, each is more than two miles tall."

The publisher of my own Journal of Economic Perspectives, the American Economic Association, decided earlier this year to make the journal freely available to all on-line--not only the most recent issues, but the archives going back 12 years or so. Thus, I read with particular interest the article draft report that Mark J. McCabe has done for the National Academy of Sciences: "Online Access and the Scientific Journal Market: An Economist’s Perspective." Here are some of his comments, although I have omitted citations for readability.

Conclusion

"Online access to the scientific literature has transformed the distribution of the scientific literature. This literature is now easier to search and read, especially for the producers of new articles: the scientist authors affiliated with research institutions. Unfortunately, the cost of supporting this enterprise has not declined. Ironically, the same technologies that enable immediate access for readers also facilitate bundling and pricing policies by the major commercial publishers that exacerbate rather than alleviate the inflationary pricing trends of the pre-internet era."

On the "journals crisis"

"Starting in at least as far back as the 1980s, and continuing to the present day, prices for these journals have increased at rates far exceeding general inflation rates, and faster than the growth in overall library budgets. This trend and its negative impact on institutional journal collections are often referred to as the “journals crisis.” With the emergence of low-cost internet-based distribution of content in the late 1990s, as well as open access journals, there was some hope in the library community that this crisis might abate, and access prices might even decline. However, prices continued to increase at or above economy-wide rates of inflation."

How has the journal market evolved with on-line publication?

"By 2000 or so, most of the changes wrought by the internet that are visible today were in

evidence. They include:

1. Current journal content is sold primarily as part of large publisher-specific journal bundles, or

“Big Deals,”and normally includes access to content back to the 1990s. Print

is still available for a surcharge.

2. Bundle prices are institution-specific; access is sold on an annual subscription basis.

(Contrast this with the absence of price discrimination in the print era, and the lack of bundling.)

3. The emergence of commercial and non-profit open access (OA) journals. OA journals can be

accessed online at no charge, and recover their costs through some combination of author fees

and grant monies and government funding. The Directory of Open Access Journals or DOAJ currently catalogues more than 6000 titles, many of which are peer-reviewed.

4. Publisher sell their electronic journal backfiles for a one-time charge; 3rd parties provide

electronic access to backfile content from multiple publishers on an annual subscription basis,

e.g. via Ebsco or JSTOR.

5. In addition to the open access working paper repositories mentioned earlier, dozens of major

research universities and funding organizations have adopted (open access) self-archiving

mandates. (go to http://roarmap.eprints.org/ for a list of the organizations and the repository

websites).

6. Google Scholar. This search tool was not introduced until late 2004 but has quickly emerged

as a powerful complement to the content available online."

How online access to journals has entrenched incumbent publishers

"The conceptual/theoretical analyses of journal bundling discussed earlier suggest that the adoption of Big Deal contracts are likely to deter new entry (and/or encourage exit), and enhance the market power of the largest incumbent firms. In other words, although online distribution did lower distribution costs it obviously did not change the basic demand conditions in this market; if anything this new technology augments their exploitation, since it has facilitated cost effective bundling and price discrimination. The annual 7% price increases should continue until those demand conditions change."

Do articles in open access journals get more citations?

"Although open access journals have begun to proliferate, perhaps in response to publisher bundling, their long-term viability in lieu of subsidized author fees remains uncertain. One of the chief benefits of OA is supposed to be greater readership and impact (and this assumption is important in providing the economic justification for the OA business model). However, the evidence in support of this claim remains uncertain. Although initial studies of this question revealed large positive benefits of online access (including open access), more recent papers on this subject have identified a series of data and econometric problems that when addressed eliminate most but not all of the presumed benefits."

If one accepts the argument that the supply of skilled workers in the U.S. hasn't been keeping up with demand in recent decades, and further accepts the argument that a skilled workforce is essential to future growth in a nation's standard of living, it's troubling to observe that the America's long-standing advantage in sending more of its people on to higher education is evaporating. For example, in a report out last month from the Georgetown University Center on Education and the Workforce, Anthony P. Carnevale and Stephen J. Rose write: "A clear trend has emerged: The United States is losing ground in postsecondary education relative to our competitors. ... The significance of these rankings goes beyond mere bragging rights—increasing our supply of skilled labor is central to the vitality of the U.S. economy."

Carnevale and Rose illustrate the point with two figures. The first one shows the share of those in the age 25-64 age bracket who have college degrees (including both two-year and four-year degrees). The U.S. ranks near the top, with Japan and Canada. But if one looks at another figure, this time showing only those in the younger 25-34 age bracket, one sees that the U.S. advantage in college attainment is concentrated in older age groups. The U.S. is only middle-of-the-pack in attainment of college degrees among high-income countries.

In the Summer 2008 issue of my own Journal of Economic Perspectives, Elizabeth Cascio, Damon Clark, and Nora Gordon make a similar point in "Education and the Age Profile of Literacy into Adulthood." They write: "For most of the twentieth century, the United States led the developed world in participation and completion of higher education. ... In recent years, however, other high-income countries—many of which established comprehensive secondary schooling in decades prior—have substantially expanded access to university education. In fact, many countries that significantly lagged the United States in university graduation only a decade ago—Finland, Sweden, and the United Kingdom among others— now have comparable

if not higher graduation rates."

They offer a table showing that in 1970, the U.S. led most countries of the world in (four-year) university graduation rates, and often by a lot. By 2004, lots of other high-income countries had closed the gap.

Carnevale and Rose point out that on current trends, the number of U.S. workers with a post-secondary education will rise by 8 million by 2025, and argue that the U.S. should set a goal of adding an additional 12 million workers with post-secondary education over that time. The goal seems worthy enough, but the devil is in the details. After all, the true challenge isn't to hand out an extra 12 million college diplomas, but to raise the education level of high school students so that more of them are ready to attend college, and to reform higher education to get costs under control and assure that it is adding to the skill sets of students, broadly understood.

There's a lot of cynicism these days about U.S. higher education, about whether the ever-rising costs are worth the benefits. I live and work in higher education, and there is plenty of room for reform. But whatever one's doubts about the current state of U.S. higher education, watching the U.S. lose its historical advantage over other high-income countries in terms of what share of the population gets a college degree is deeply troubling.

They write: "The relative wages of college-educated workers have been rising much faster than the wages of

people with a high school diploma. The laws of supply and demand are the best single indicator of whether the United States is producing enough, too few, or too many college graduates. If the relative earnings of college-educated workers rise faster than the earnings of their counterparts, it means the demand is growing faster than supply. The data, therefore, are unequivocal—Americans are undereducated."

To illustrate this theme, they present a couple of useful figures from the 2008 book by Claudia Goldin and Larry Katz: The Race Between Education and Technology. The first figure shows how supply and demand of college-educated workers has evolved over time, compared to the 1970 levels. The general pattern is that demand for these skilled workers was ahead of supply in the 1920s, supply then went ahead of demand most of the time up until about 1980, and since then demand for skilled labor has outstripped supply.

The next figure shows the "wage premium"--that is, how much more is skilled labor paid over unskilled labor. In this figure, “skilled labor” is defined as all holders of four-year college degrees and graduate degrees, plus one-half of those with some postsecondary education, while "unskilled labor” those who did not complete high school, those with only a high school degree, and the other half of those with some postsecondary education.

When demand for skilled labor outstrips supply, then the wage premium for skilled labor is high. When supply outstrips demand, the wage premium for skilled labor drops. This is a powerful explanation for why inequality of incomes has changed over time.

But while I'm sure this argument is a lot of the explanation for rising inequality, maybe most of the explanation, other issues play a role as well. For example, the demand for skilled and unskilled labor is also affected by factors like the great advances in information and communications technology in recent decades, and by the ability of firms to outsource some kinds of production to other countries. In addition, the evidence on income inequality from my post last week suggests that a lot of the rise in inequality is because of gains going to the very top of the income distribution--not necessarily broadly distributed to all of those with a higher level of education. So puzzles about the causes of inequality remain.

The report is called "Price Volatility in Food and Agricultural Markets: Policy Responses." It describes the situation of global prices in agricultural products over the last few years like this:

"Irrespective of any conclusion that might be drawn concerning the long term trends, there is no doubt that the period since 2006 has been one of extraordinary volatility. Prices rose sharply in 2006 and 2007, peaking in the second half of 2007 for some products and in the first half of 2008 for others. For some products the run-up between the average of 2005 and the peak was several hundred percent. On the rice market the price explosion was particularly pronounced. The price rises caused grave hardship among the poor and were a major factor in the increase in the number of hungry people to more than one billion.8 Prices then fell sharply in the second half of 2008, although in virtually all cases they remained at or above the levels in the period just before the run-up of prices began. Market tensions emerged again during 2010 and there have been sharp rises in some food prices. By early 2011, the FAO's food price index was again at the level reached at the peak of the crisis in 2008 and fears emerged that a repeat of the 2008 crisis was underway."

The 10 agencies point to a number of factors affecting food prices: growing world population and incomes, weather-related disruptions, and others. But then they focus quite particularly on biofuels subsidies (I've dropped footnotes and paragraph numbers from the quotation that follows).

"Between 2000 and 2009, global output of bio-ethanol quadrupled and production of biodiesel increased tenfold; in OECD countries at least this has been largely driven by government support policies. ... Biofuels overall now account for a significant part of global use of a number of crops. On average, in the 2007-09 period that share was 20% in the case of sugar cane, 9% for both oilseeds and coarse grains (although biofuel production from these crops generates by-products that are used as animal feed), and 4% for sugar beet. With such weights of biofuels in the supply-demand balance for the products concerned, it is not surprising that world market prices of these products (and their substitutes) are substantially higher than they would be if no biofuels were produced. Biofuels also influence products that do not play much of a role as feedstocks, for example wheat, because of the close relations between crops on both the demand side (because of substitutability in consumption) and the supply side (due to competition for land and other inputs).

"At the international level, crop prices are increasingly related to oil prices in a discrete manner determined by the level of biofuel production costs. ... Since both energy and food/feed utilise the same input, for example grain or sugarcane, increases in the production of ethanol reduce the supply of food and result in increases in its price. This relationship between the prices of oil, biofuels and crops arises due to the fact that, in the short run, the supply of crops cannot be expanded to meet the demand by both food and energy consumers.

"If oil prices are high and a crop's value in the energy market exceeds that in the food market, crops will be diverted to the production of biofuels which will increase the price of food (up to the limit determined by the capacity of conventional cars to use biofuels - in the absence of flexfuel cars and a suitable distribution network). Changes in the price of oil can be abrupt and may cause increased food price volatility. Support to the biofuel industry also plays a role. Subsidies to first-generation biofuel production lower biofuel production costs and, therefore, increase the dependence of crop prices on the price of oil. Such policies warrant reconsideration."

And so the 10 international agencies offer what strikes me, by the standards of these kinds of reports, as a shockingly blunt recommendation:

"Recommendation 6: G20 governments remove provisions of current national policies that subsidize (or mandate) biofuels production or consumption."

When looking for statistics on U.S. income inequality, my standard starting point is the data from the U.S. Department of the Census, which shows the share of income received by each quintile (that is, each fifth) of the income distribution, as well as the share received by the top 5% of the income distribution.

(Specifically, see Table F-2 at this link.)

The basic story is that the income distribution didn't move too much from the mid-1950s up to about the mid-1970s; indeed, when I was learning economics in college in the late 1970s and early 1980s, a rule of thumb was that the U.S. income distribution was essentially stable. But since then, the share of income going to the top fifth has risen substantially, from 40.7% of all income in 1975 to 48.2% of all income in 2009. That increase of 7.5 percentage points is almost all traceable to the top 5%, which saw its share of total income rise by 5.8 percentage points over this time--that is, from 14.9% of total income in 1975 to 20.7% of income in 2009. Over this time, the "fourth fifth" of the income got a slightly smaller share, and the bottom three-fifths all saw a substantial decline in their share of total income.

In an essay in the March 2011 issue of the Journal of Economic Literature, Anthony Atkinson, Thomas Piketty, and Emmanuel Saez write about "Top Incomes in the Long-Run of History." (An ungated version of the paper is available at Saez's website here.) They use tax data to construct estimates of income inequality in the U.S. and other countries going back to early in the 20th century. The tax data isn't directly comparable to the Census data just mentioned, but it's the only reliable source of data on the very top of the income distribution going back this far in time. The paper is long and chock-full of insights, but here are a few of their basic facts on U.S. income equality over time.

First look at the share of income going to the top decile--that is, the top tenth--of the income distribution. This follows a U-shaped pattern: after rising in the 1920s, the share of income going to the top tenth drops in the Depression, stays relatively fixed from the 1940s up through the 1970s, and rises since then.

Now, break down that top tenth into three parts: the top 1%--the solid triangles in the graph; the next 4%-- that is, from the 95th up to the 99th percentile--which is the hollow triangles in the graph; and the next 5% after that--that is, from the 90th to the 95th percentile--which is the hollow diamonds in the graph. It turns out that most of the increase in the share of income received by the top 10% is actually a rise in the share being received by the top 1%.

Finally, look not at the top 1%, but at the share of income received by the top one-tenth of 1%. Remarkably, it turns out that a large share of the growth in inequality is because of growth in the share of income received by this tiny sliver of the income distribution.

How bothersome is the level of inequality we have reached in the United States, and the concentration of that inequality in the extreme upper part of the income distribution? There is of course great controversy on this point. After all, these figures are annual snapshots, and don't show mobility across income levels between years. Probably the top 0.1% of the income distribution varies considerably from year to year, depending on which executives are cashing in a lifetime's worth of stock options in a single year. At the bottom end of the income distribution, income statistics don't take into account the value of "in-kind" transfers like Medicaid, Food Stamps, or vouchers for low-income housing. There are questions about how well tax data captures the overall income distribution at different historical points in time. There are a variety of arguments over why this trend toward great inequality has happened, many of them emphasizing how changes in information and communications technology have allowed those with high skills to increase their earnings.

For now, I'll duck these issues and controversies , and just let the fact that I think these data are worth presenting speak for itself. We can debate what the facts mean, but it IS a fact that in historical terms, U.S. income inequality is currently very high, about as high as it has been in the last century. It is also a fact that most of that change in inequality is because of a larger share of income going to the very top of the income distribution.

Kevin J. Lansing of the San Francisco Fed offer some graphs that illustrate the severity of the Great Recession: one compares the decline in real household consumption per person in the 2007-2009 recession to the recessions of 2001 and 1990-91; another compares the decline in real household net worth per person in these three recessions.

Lansing offers an additional figure worth contemplating: the change in the employment/population ratio since 1988. The unemployment rate has some well-known difficulties as a measure of the employment situation: for example, "discouraged" workers who have given up looking for jobs are not counted as officially unemployed, but rather as out of the labor force. But the employment/population ratio is just based on dividing two numbers--employment and population. The shaded areas in the figure show periods of recession, when the employment/population ratio does tend to fall.

But the decline in the employment/population ratio in this recession is enormous: 5.2 percentage points over four and a half years: from 63.4% in December 2006 to 58.2% in June 2011. Back in the grim double-dip recession of the early 1980s, for comparison, the employment/population ratio fell 3 percentage points over a bit more than three years, from 60.1% in December 1979 to 57.1% in March 1983.

These enormous declines in consumption and in asset values and the loss of jobs, of course, help to explain why the economic "recovery" is sometimes being called the Long Slump. The pattern also offers some background as to why the federal budget talks seem so intractable: when a recession dents the economy this badly, passions are going to run high.

Private capital is, on net, flowing from advanced economies to emerging economies. However, even larger flows of public capital are, on net, flowing in the other direction from emerging economies to advanced economies. Here's a figure to illustrate the point, from Simona E. Cociuba of the Dallas Federal Reserve:

These "upstream" capital flows--that is, from middle-income to higher-income economies--won't go on forever. At some point, countries in the rest of the world will not wish to expand their holdings of foreign and especially U.S. dollar assets further.

But the pattern of the U.S. economy investing overseas in somewhat riskier private assets, while foreign governments and investors stock up on safe U.S. assets like Treasury bonds, may be a pattern that lasts for a long time. As I learned from an article by Richard Cooper on trade imbalances in the Summer 2008 issue of my own Journal of Economic Perspectives, even though foreign investors own more in U.S. assets than U.S. investors own in foreign assets, U.S. investors receive larger cash flows from their foreign assets than do foreign investors from their U.S. assets.

In 2009, for example, total U.S.-owned assets abroad were $18.3 trillion, while total foreign-owned assets in the U.S. were $21.1 trillion. However, the U.S. economy as a whole received $165 billion in receipts and payments from its assets abroad, while the foreign investors received $124 billion in receipts and payments from their U.S. investments.

How is the U.S. economy getting higher payments from a lower total pile of assets? A more detailed look at those assets suggests and answer. More of the foreign assets are in low-earning safe havens like Treasury securities, while more of the U.S. assets abroad are direct ownership of assets or equity. For example, the U.S. has more direct investment abroad ($4 trillion) than the foreign-owned direct investment in the United States ($2.7 trillion). Similarly, U.S. investors owns more corporate stock abroad ($4 trillion) than foreign-ownership of corporate stocks in the U.S. ($2.4 trillion).(All statistics in these last two paragraphs are from tables B-103 and B-107 from the back of the 2011 Economic Report of the President.)

There is a long-term advantage here for the U.S. economy, based on its financial and legal structure, and its investment and managerial expertise. In a metaphorical sense, the U.S. economy operates like a huge bank, accepting "deposits" from the rest of the world on which it pays fixed safe interest rates, and then seeking ways to invest that money in corporate projects around the world.

{kind=link}

{kind=link}